Below is my letter for 2021 Q2, in which I shared my thoughts on Chinese political & economic system, and its implication on regulatory impact on our portfolio companies.

China

Investor Letter – 2021 Q1

Below is my letter for 2021 Q1, in which I shared my thoughts concerning Chinese education businesses and commented on new positions of Tianli Education (1773.HK), TAL Education (TAL) & Futu Holdings (FUTU).

China Meidong Auto (1268.HK)

Below are excerpts from our 2019 Q3 letter regarding our new position Meidong Auto, for easier reference purpose.

Also, attaching the letter to shareholders from its 2018 annual report, it’s quite a good read: MeidongAuto_2018_Letter

Meidong Auto is a new position from the “Great Operation at Reasonable Price” category. It doesn’t come often that a CEO’s shareholder letter alone made me think seriously to become a shareholder. Meidong had made to this list. In short, it is a easy to understand business (luxury auto dealer), who had an exceptional “outsider” CEO who was able to communicate transparently and sincerely about its strategy and execution. It has been executing its strategy very well, generating excellent return on equity (25+%) over past 3 years.

Meteorology: China has seen its auto market slowing down after a few years of high growth. Luxury car however still enjoyed healthy growth. According to CPCA’s data, luxury brands have maintained a 10~% annual growth rate from 2016 to 2018 (while overall auto market observed +13.9%, 3% & -2.8% for the same three years respectively). Furthermore, CPCA’s most recent July 2019 data even shows an accelerating +24% yoy growth rate for luxury cars. This trend, while perplexing, could be explained by the secular shift of the consumption power in China (from tier 1 cities to lower tier ones, & a growing middle class in all tiers cities, etc.) and further inequality in wealth distribution.

Topography: Meidong uniquely chose to position as the sole dealer of a luxury brand in tier 3-4 cities. Such position allows Meidong to earn a high gross margin (on average about 100 bps higher than multileader in a city) due to weak competition. Such position also increased the stickiness of lucrative after sale service business. it however is a narrow moat because if competitors really want to imitate this strategy, they could achieve so and drive the margin down. In terms of the sustainability of such narrow moat, I think it is still in good position at least for short term (2-3 years), based on our evaluation of incumbents (who are at least a few years behind Meidong’s business principles & executions).

Commander: The management of Meidong is the most impressive factor. In fact, the CEO Ye Tao, reminds me the CEOs from William Thorndike’s book “The Outsiders”. Ye Tao has technical backgrounds, graduated from MIT with both engineering and MBA degrees, also served as executives to various software business in United States & in Asia. The way Ye Tao approaches car dealing business can be described as quite “rational”, which can be seen by reading a single shareholder letter from him. Ye Tao think the most important principles of his business are 1) high inventory turnover, 2) grow service revenue (the high margin business) & 3) focus on new store ROI. It may worth quoting directly from its 2018 letter. On the inventory turnover, it is refreshing to read something like “We live or die by inventory turns. Fast-turns make us a cash printing machine; slow-turns turn us into a cash-sucking black hole.” In addition to the principles laid out, the company’s reporting also provides metrics to track how they performed in these three areas. On capital allocation, the management preferred to use dividends. That 4 is not the most favorable way of distribution value back to shareholders, given the price is still a bit underpriced in my opinion.

System: One thing to note is that Meidong is still very closely held by insiders. 65% of the shares are held by the family trust of Ye’s brothers.

Valuation: we have built a material position at about 12x 2019 est. earning, a reasonable price for such a high-quality business.

China Internet Report 2019

I want to share a great overview study of China tech industry landscape of 2019 by South China Morning Post & Abacus. I think the advanced AI usage by Chinese tech companies are highly under-appreciated by the outside world.

This study has many live evidences of what Kai-Fu Lee wrote/predicted in his latest book “AI Superpowers: China, Silicon Valley, and the New World Order” which I recently just finished. Highly recommended and will try to do a review later.

Another interesting trend particularly interests me is the integration of live streaming and shopping. I think this model (temporarily dubbed it as “QVC on steroid” for the sake of western world readers’ familiarity) has huge potential and I plan to study it more.

Quick review of Chinese Tech Stock selloff – what does Mr. Market know that you don’t

Chinese tech names are hit hard in the past few months. As holders of a handful of them, I’m curious to know what Mr. Market knows about them that I don’t.

Starting with Tencent, game monetization approval is indefinitely halted, corporate structure is shaking up. Maybe that’s why it lost 38% of its value in past 180 days. How about JD? Founder CEO Richard Liu got into this sexual assault scandal. That must be why it lost 48%% of its market value. YY? Oh, that must be because the new type of short video, e.g. Douyin/Tik Tok gaining traction leading to it’s 43%% market valuation evaporation. BABA? Jack Ma retiring must lead to 34% market value drop.

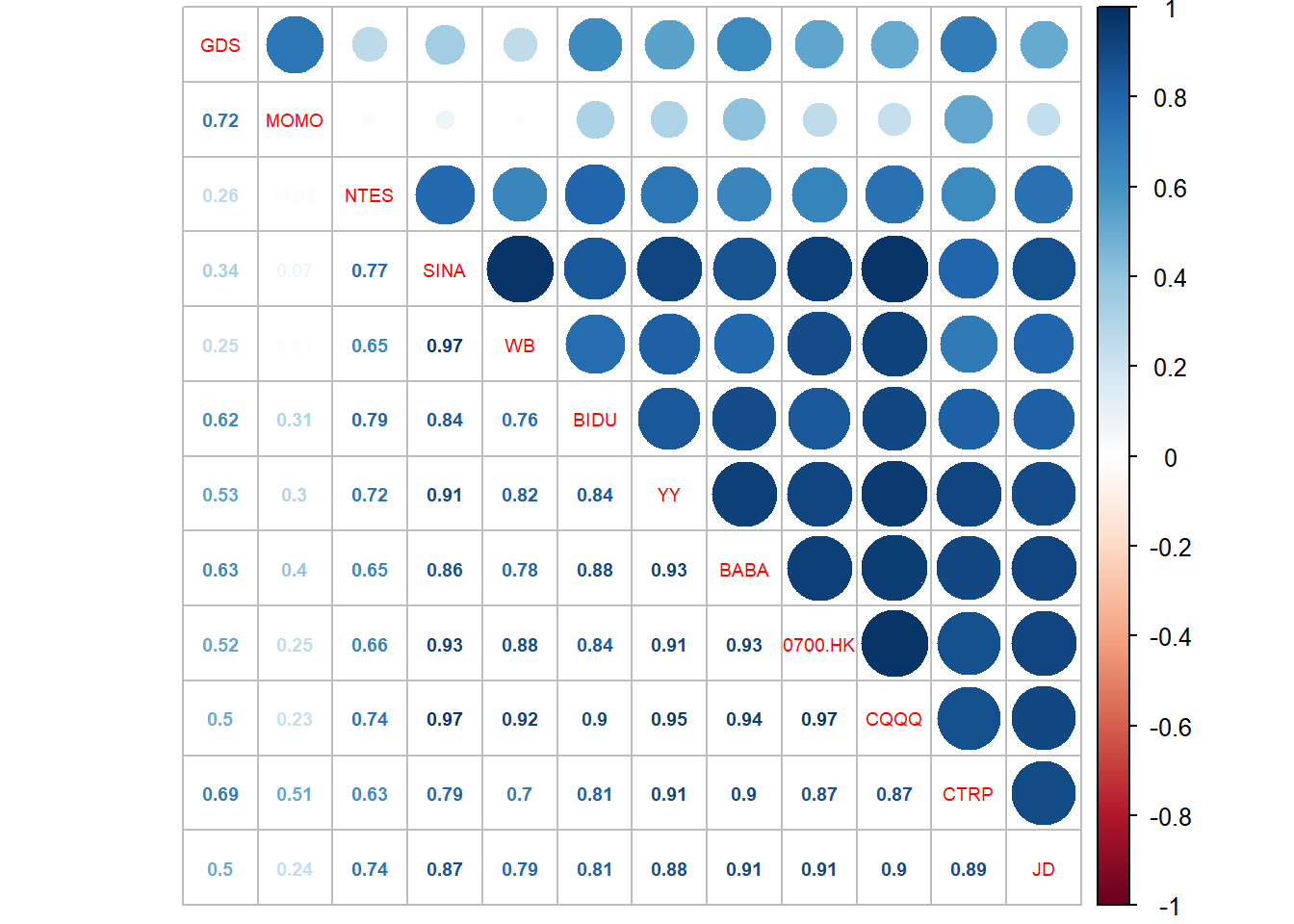

Well, if they are plausible, what about BIDU, WB, NTES, MOMO, SINA, CTRP & GDS who all happened to lose 30-50% from their recent high? Are there plausible fundamental reasons to explain each of them incurring so similar negative returns? I’m sure financial journalist could help find them if they want to. However, it looks to me such synchronized movements could hardly be explained well by idiosyncratic risks. I just want to see how much these movements are synchronized (correlated), thus can be attributed to market as a whole, rather than for each specific name.

I’m a R person, and below I try to do some simple statistic summary. I also attached my R scripts in markdown file for whomever is familiar with R and may want to play around with it.

Download R Markdown Notes: Link

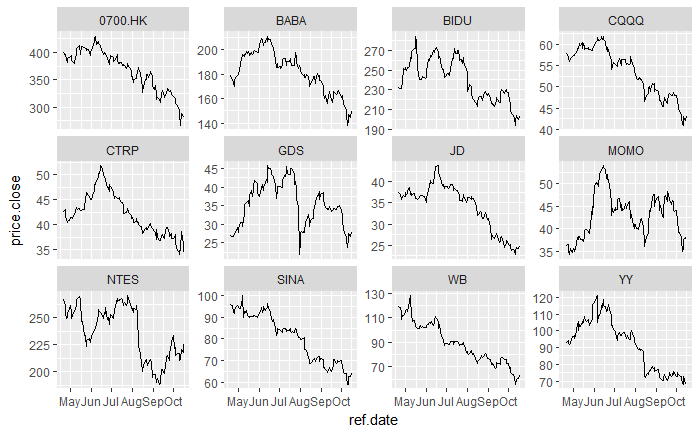

- Here is how daily close price looks in past 180 trading days:

- Here is the performance and max drawdown in same period

- here is the correlation matrix & its visualization

All these large blue dots indicate highly correlated daily price movement between these names, as well between single names and CQQQ (a Chinese tech ETF).

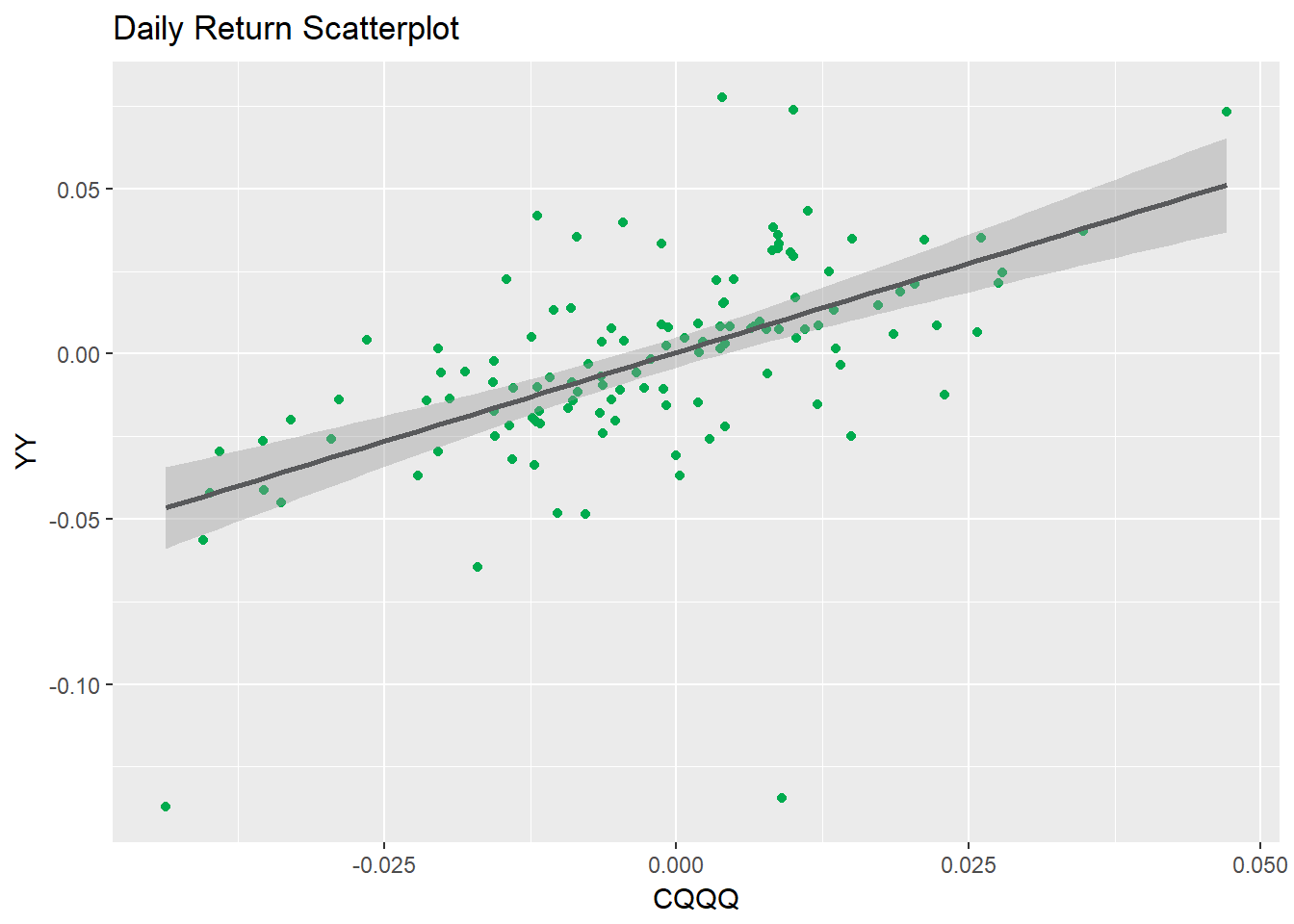

- Let’s try to do a linear regression for YY to see how we can use CQQQ’s return to explain YY’s.

First, scatterplot the return of them, the best fit line already looks positive and close to 1.

Based on below linear model, slope of CQQQ is highly statistically significant (p value basically is 0). In other words, CQQQ’s return has high power to explain YY’s return. Note YY is less than 3% of CQQQ’s holdings.

![]()

In conclusion, my interpretation is that Mr. Market may not know more about each of these individual company than I do, rather it may be more driven by overall fear to macro events.

Shoulders of Giants – Charlie Munger & Li Lu Interview 08/2018

Note: I have shared these videos via my Twitter account before, however may have missed readers who only follow the blog. Copyright of Weekly in Stocks, all contents are shared for non-commercial knowledge sharing purpose.

These are interviews conducted by a Chinese finance/business media called Weekly in Stocks. Overall, I really enjoyed it and think all questions are really well prepared. As expected, many questions are around China (both philosophy & capital markets).

I think this might be the first time Munger explicitly drew parallel between his & Buffett’s philosophy & practices and oriental philosophies. Quoting from Munger: “…why are these people in China so interested in Berkshire Hathaway and Charlie Munger… and why do the Chinese like the book (Poor Charlie’s Almanack), I think the answer is it sounds Confucian…”, “…If you are a better person, you are likely to be a better investor; If you are a wiser person, you are likely to be a better investor…”

The follow-up interview with Li Lu alone is also of great interest, where he, may be for the first time, talked in details about Munger’s life, their interactions & his lessons learned from Munger, as well as his unique views of Chinese capital market.

Interview with Charlie Munger along with Li Lu [3 parts]

Follow-up Interview with Li Lu [2 parts]

YY – an Under-Followed Chinese TMT Play with Margin of Safety

YY is a Chinese video live streaming + social networking business with two main operational segments, YY Live (the general entertainment content streaming, a loose equivalent of Periscope) and Huya (Gaming content streaming, an equivalent of Twitch). Its share has risen 135% YTD and valuation moved from a dirt cheap 11 trailing P/E by 2016 to a less cheap trailing 16 P/E (still cheap compared to other Chinese Tech peers), so why I am still interested in this name?

In short, a debt-free cash-gushing main business poised to take more market share as the general entertainment streaming market start to mature and consolidate, plus a fast growing gaming/e-sports streaming platform close to turn profitable and filing IPO in a favorable secular tailwind should warrant a market average valuation. In addition, I noticed both platforms achieved market leading positions without promotion and successfully fended off competitors who tried to copy their business model. Add to it, YY has a deep-thinking founder-CEO with some track records of continuous innovation in fast changing market environment. All in all, this is something I think should be priced at a premium to market. My neutral assumption based valuation shows there still could be 29% upside, and a conservative assumption based valuation shows 0% downside. (optimistic assumption indicates 90% upside, but I don’t have to count on it)

Great Oriental Investors – Shoucheng Zhang, a Quantum Polymath (Award Winning Physicist and VC Investor at once)

As I mentioned in my first investor letter, my investing philosophy had deep roots in oriental philosophies. For this reason, I always find those investors who are able to master both eastern and western mental models extremely intriguing. On surface, lots of eastern mental models & philosophies resonate with well-known western principles already, but I also believe they have more unrecognized value to investing practices. I am planning to start a series to document all investors that fits this category, to document my lessons learned from them and to share with my readers their insights (many of which aren’t available in English media).

The first one is Shoucheng Zhang (Wikipedia Link). Zhang is an ingenious physicist, to say the least. He got admitted by one of the top universities in China purely by self-study after the Culture Revolution ended in 1978 when he was only 15, then went abroad and finished his PhD by 24. His best known finding is probably topological insulators, for which he was awarded a Dirac Medal in 2012. His work was estimated by Thompson Reuters to be able to win Nobel Prize in 2014 (Link). Zhang is also a tech VC investor. He is said to be one of the early investors of VMWare (as he’s a neighbor of the co-founder Mendel Rosenblum who is also a Stanford professor) and made hundred bagger on it. He officially started his profession investing career in 2013 by founding Danhua Capital (website link), an early/growth stage VC focusing on disruptive technologies.

Like Charlie Munger, Zhang also see Benjamin Franklin as an archetype. Zhang mentioned that he struggled at a young age on whether he should aspire to be a scientist or an entrepreneur, until he realized he really could be both after reading about Franklin, one of the greatest polymaths in history. Not surprisingly, he is also a fan of multi-disciplinary mental models. As a theoretical physicist, his application of quantum physics principles to investing (and life) is the most interesting insights among other thing. Additionally, contradicting to stereotype of physicists, he seems to have strong interests in Aesthetics.

Zhang’s key philosophy can be summarized by a quote he constantly mentioned in multiple interviews: “Complexity out of Simplicity” or “First Principle”. Before moving on, I think it would be beneficial to expand on the “First Principle” (Wikipedia link) as it initially appeared foreign to me. My understanding is that first principle is a thing/principle/notion which is in its most fundamental form and is self-evident without proof or deduction. That is where you want to start your learning/thinking process.

Some of my favorite thoughts of Zhang (paraphrased) are below:

Chinese ADR “Go-Private” Deals Overview- A Changyou Buyout Inspired Study

On 5/22/2017, Changyou [CYOU] received a preliminary non-binding offer from its chairman Dr. Charles Zhang, who is also the CEO and Chairman of Changyou’s parent company Sohu, to take the company private with and offer of $42.10 per ADS. The offer letter can be seen here: http://ir.changyou.com/05_22_2017.shtml. It is interesting that it is Charles Zhang, the person, not the parent company Sohu, to make the acquisition.

As a current CYOU shareholder, I think it’s a OK deal despite I had higher expectation of the turnaround execution which just started to show some positive signs. As of 5/31/2017, there is still about 8% spread between the close price of $38.9 and offer price $42.1. If the deal could be closed timely, it would be a good risk arbitrage opportunity.

Inspired by this event, below I did a general study of all the Chinese ADR “go-private” deals in past few years. I’m keen to get answers to these 3 questions (which could help me evaluate upcoming similar deals’ risk/reward):

- How much percent of these deals fell through?

- What are the characteristics of the failed deals? (does CYOU have any of these traits?)

- How long do they usually take to close?

History of Chinese ADR Privatization Deals

Let’s begin with a rough understanding of a typical ADR privatization process. Credit to a Credit Suisse’s study [link here], here is a great chart showing the 6 milestones of such a process.

It is also important to understand the main incentive of such privatization deals, specifically for these US listed Chinese companies. Like most of the PE backed LBO deals, Chinese ADR privatization deals also target for a relist for higher valuation. However the difference is that, rather than streamlining and growing the businesses for a few year in private arms (in LBO cases), the Chinese ADR companies could seek a faster re-valuation by relisting the firm to its home market (which offered richer valuation, especially back in 2015 before the crash). This also explained why there were so many proposed deals announced in 2015.

Texwinca (0321.HK) – a Cigar Butt or Anything More?

Disclosure: I do not hold position in mentioned stock. Also, the price has increased slightly since I initially wrote it up (from HK$5.11 to HK$5.30), however all points in this write up are still valid with a price level of HK$5.30.

Company Overview and Recent History

Texwinca is a Hong Kong-listed textile & apparel company, with two main business segments: 1) Textile business, which produces, dyes & sells knitted fabric and yarn, & 2) Retail and distribution business, which sells casual apparel and accessories. Each segment contributes about the half of the revenue to the firm. The vertically integrated cost-efficient model used to work well, however both segments have been hit hard by some adversity recently.

Texwinca’s textile business is one of the largest fabric producers in the world, serving many global fashion brands like A&F, Ralph Loren and Gap. However, it is facing cyclical headwind driven by the soft global (especially US, which is the main textile revenue source) economy and the increasing production cost in mainland China.

The retail business sells its apparel majorly through brand Baleno. However, Baleno (along with many other local mainstreet fashion brands like Esprit, Giordano & Meters/bonwe) has been squeezed very hard in its mainland China market (its main retail revenue source) by new-entering international fast fashion brands like Zara, H&M and Uniqlo. Baleno, once a high end fashion brand, lost its value significantly in the past few years, and is now considered merely as an “immigration worker (lowest income city worker from rural area) brand”. To cope with the competition, the business tried to streamline by disposing all the non-core brands and focus solely on Baleno.

Driven by weak performance on both sides, the stock has lost more than 40% of its value since the recent peak at HKD 9.38 in July 2015. At the current stock price (5.11), the stock looks attractive from first glance with following traits: