YY is a Chinese video live streaming + social networking business with two main operational segments, YY Live (the general entertainment content streaming, a loose equivalent of Periscope) and Huya (Gaming content streaming, an equivalent of Twitch). Its share has risen 135% YTD and valuation moved from a dirt cheap 11 trailing P/E by 2016 to a less cheap trailing 16 P/E (still cheap compared to other Chinese Tech peers), so why I am still interested in this name?

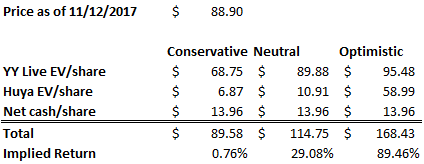

In short, a debt-free cash-gushing main business poised to take more market share as the general entertainment streaming market start to mature and consolidate, plus a fast growing gaming/e-sports streaming platform close to turn profitable and filing IPO in a favorable secular tailwind should warrant a market average valuation. In addition, I noticed both platforms achieved market leading positions without promotion and successfully fended off competitors who tried to copy their business model. Add to it, YY has a deep-thinking founder-CEO with some track records of continuous innovation in fast changing market environment. All in all, this is something I think should be priced at a premium to market. My neutral assumption based valuation shows there still could be 29% upside, and a conservative assumption based valuation shows 0% downside. (optimistic assumption indicates 90% upside, but I don’t have to count on it)

Tao

Purpose – in the most fundamental form, live streaming company is an intermediary distributing entertainment content from creator (mostly user generated) to end users. The content creates pleasure of end users, for which the creator is rewarded either by end users directly or advertisement spending of sponsors indirectly. In general, the distributors take a cut for their efforts in distributing the content. This is the same model as traditional TV/Radio/Movie broadcasting businesses. Different than traditional entertainment intermediary, streaming allows grassroots to produce and distribute entertainment content in an inexpensive way, thus opening up a brand new addressable market.

Value to all constituents – for content creators, the value is obvious, streaming businesses enables more ordinary people to monetize their specific talents which they wouldn’t be able to otherwise. To the users, the value in the pleasure of watching such content as long as the pricing is fair. For society, it also helps effectively redistributes social wealth to underdeveloped area. An anecdotal example is that 3 Chinese Northeastern provinces, which had dying heavy industrial businesses and highest young adult unemployment rates, had the largest portion of the top-paid hosts (content creators) among the country. As it creates inexpensive and accessible entrepreneurship opportunities for unemployed, it also helps stabilize the society which is the top 1 priority in Chinese government.

Morality – YY’s business model, similar to many social network models (including Facebook), is subject to a practiceI called “profit on human vulnerability”. Essentially, it sucks the users’ attention/time which could be used to other more value-producing activity, and monetize the attention via advertisement or users’ payment directly. YY’s model is, to some extent, inferior (to the society) than Facebook because it earns directly from users. More recently, there is numerous news covering adolescents, lacking of self-control, spent parents’ hard earned money on tipping live streaming hosts over-generously. However, my view to this point is more neutralized after examining the “reasonable” profit margin of broadcasting business. Taking operating margin from a few mid cap US TV/Radio broadcasting pure plays (Sinclair SBGI, Nexstar NXST & TEGNA TGNA), they are all around 30%. YY Live’s operating margin is at the same lever. This, to me, means that YY is actually taking a “fair” share for the value it provides to the society. The only difference is that, YY’s profit is more concentrated in these high-paying users, and not as spread-out as traditional broadcasters. Overtime, the distribution of the revenue base of YY may change, but I believe the 30% operating margin is reasonable and sustainable.

Vision – I believe the management has long term vision of cultivating a new industry, for which I will further elaborated it in “Commander” section below.

Meteorology

Anyone have some exposure to Chinese social live in recent years would not disagree on favorable secular trend for streaming businesses. The real question is how sustainable is the tailwind. My general view is that although certain forms of entertainment may be “faddish”, this type of inclusive and interactive entertainment ecosystem is not faddish, thus the distributor role like YY should be here to stay.

Various market researches show that entertainment streaming industry is getting close to a mature (i.e. relatively slow growing) stage. According to CNNIC, online streaming user counts reached 344 million by 2016, a penetration of 47.1%. Credit Suisse research predicts total market to be $5 billion by 2017 and a much lower (still low double digits though) growth in near term.

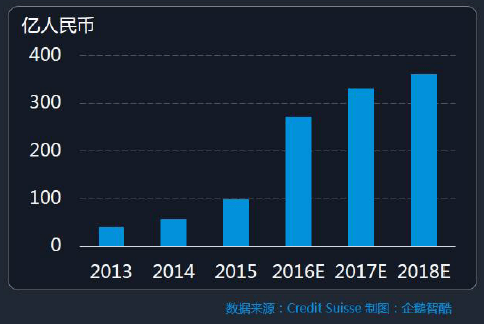

Gaming streaming industry, on the other hand is generally believed still in its fast-growing stage (See blow chart from local market research firm Analysys). Another market research consultant iResearch believe the total market could reach RMB 3 billion ($450million) by 2018. One key difference is that content creator in gaming streaming (professional gamers & tournament organizations) currently had much stronger pricing power than general entertainment content creator. This is a main reason most gaming streaming businesses are still unprofitable when they still rely on an end-user-paying revenue model (high COGS, low gross margin). I think the long-term profitability of this industry depends on the standardization of the gaming events and extensively introducing business sponsors into the value chain. Looking at traditional sports, professional athletes physically don’t need that much rest between halves/quarters/innings, it is the sponsors/advertisers who really need these time breaks. In long run, I believe gaming/e-sports industry should be able to expand its addressable markets significantly and streaming business as distributor should be able achieve similar profit margin as traditional sports content distributors, if not better.

YY has two main operation segments, YY Live (general entertainment) and Huya (Gaming). Specific for YY’s competitive landscape, I see both platforms among leading pack in their own industry.

For general entertainment, YY Live posted Q/Q revenue growth -11% & 15% in Q1 & Q2 2017 (Q1 is cyclically weak due to Chinese New Year). Compared to same quarters last year, the Y/Y growth rates are 24% & 19% for Q1 and Q2 2017 respectively. It should also be noted that street estimate revenue of 17 to be over RMB 10 billion which is almost 1/3 of the total market. When the market matures (growth slows down), all the not-profitable platforms will eventually go out of business and I believe YY is poised to take these traffic as the industry leader.

Huya had an impressive Q/Q growth streak, posting 22%, 38%, 72%, 18% & 16% topline Q/Q growth from 2016Q2 to 2017Q2. Its market share measured by MAU is stacking 3rd after Douyu and PandaTV. It should be mentioned that Huya still only used about 5% on Sales and Marketing during this period. Since Douyu and PandaTV are both private companies, I couldn’t find actual S&M spending. Anecdotally, I think they spent much more on marketing based on their commercial presence & related news. In my opinion, although the TAM for gaming streaming could be much larger than market research firms’ estimate, the market shares for each player would be heavily driven by the content itself (rather than community culture for general entertainment streaming) so the competition for quality content will be fierce in following years. I believe YY management also realize it, that’s why they sought capital market for $75m Series A in May 2017, a secondary offering of YY for $400m in Aug 2017 and a potential spinoff IPO of Huya in near term. If management is able to use raised proceeds to build up content moat (even though temporarily depressing gross margin), that would be a great execution. On side thinking, I believe game developers of these competitive games (EA, Activision Blizzard, Tencent & NetEase, etc.) could have a much larger TAM if e-sports come to mainstream. Just imagine how much the inventor of soccer, suppose there is such a one, can take from FIFA every year…

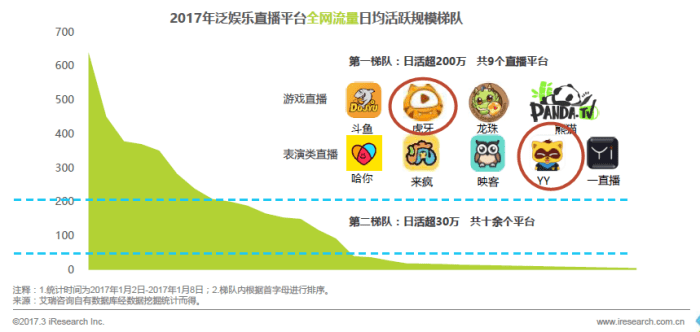

The first one below iResearch report shows both YY Live and Huya are among top players based on daily active users (DAU) from 1/2/2017 to 1/8/2017. The second Cheetah Data report shows both YY Live and Huya are #1 and #2 platforms based on weekly active penetration (Android platform only) during Q3 2017.

Topography

Moat

Statistically, YY produced average ROE 40% and ROIC 30% in the past 5 years. By and large, business with such return numbers in a 5 years period has some sort of moat.

In my opinion, there are two angles, both of which are related to “culture” of YY’s platform.

1) Best in class PGC/UGC created by best in class host groups. This can be verified by how low S&M spending (3%, 5% & 5% for 2014, 2015 & 2016) compared to revenue growth (102%, 60% & 39% for 2014, 2015 & 2016). What it says is that YY really achieved such impressive topline growth by mainly word of mouth. This is even more impressive when considering many competitors came in to the space circa 2015 and burned piles of cash to acquire traffic.

2) Stronger user stickiness and spending culture creates a virtuous circle to attract more quality hosts and more users. Rather than directly spending on user acquisition, YY’s growth strategy is heavily around community building and host/user habit cultivation. The live streaming business’ core monetization model – users tipping hosts with virtual award items (which users bought from the platform), is an invention of YY back in 2014. Measured from user stickiness and spending inclination, YY is the best in class. One research [link] shows 29 out of the top 50 highest paid hosts are in YY’s platform (a 2nd or 3rd platform by MAU generates 1st revenue, that means higher ARPU).

Both factors combined, competitors cannot simply copy YY’s model and drive down YY’s profitability. A case study of the fall of once top 1 general entertainment streaming platform Yinke can show why streaming broadcasting is not simply a capital game [link]. In past two years, Yinke succeeded growing its users base quickly to surpass YY Live by practices like hiring celebrities as hosts (increasing COGS) and spending heavily in Marketing (increasing S&M expense), only to find out users acquired this way had lower stickiness and spending inclination. When the market slows down this year, Yinke had to sell controlling stake (48%, including ALL founder’s shares) to Shunya International in September 2017, it was widely perceived as a defeat (if the profitability was strong, the founder had no reason to sell). I think YY’s moat is round it’s community culture and it’s not something can be replicated in short term.

Some additional favorable topographical considerations are:

– Strong financial position: clean balance sheet with net cash

– Innovation to drive profitability: Historically, YY had done some industry-shaping innovations, which all contribute to the sustainability and profitability of the live streaming ecosystem. One mentioned before is the “tipping” interaction, the cornerstone of the whole industry. A second one can be loosely translated to “Jointed Mic” [link] allows multiple hosts to speak/sing simultaneously in the same streaming channel, which significantly increase the possibility of the entertainment forms and user stickiness. “Jointed Mic” later became an industry standard feature.

– Financial independency: Within streaming industry top players, YY is the only “independent” one. So it can remain long term perspective if they choose to. In my opinion, all other VC-backed streaming companies will fall in the trap of “grow at any cost” to meet VC set KPI (a toxic practice to grow a community, from a long term perspective).

– More optionality: Note that many promising new innovations are currently reported through YY Live line (thus depressing margin). However, I believe some of these moonshots could be future growth engine. They includes: Happy Werewolf Kill (an audio chatroom based game, ranked #1 based on active users), Tantan (Chinese version of Tinder) & Bigo Live (dominating live streaming app in Southeast Asia)

Commander

Founder and CEO David Xuelin Li is an interesting figure and I believe he deserves major credit for YY’s success thus far.

Winding clock backward 20 years, Li graduated from one of top schools in China with a philosophy degree. In the next 10 years or so, he’d been a journalist, a chief edit of a few tech magazine & major web portals (Sohu & NetEase) and then a tech entrepreneur. He’s been holding the helm of YY since it was founded by him in 2005. The main business model of YY had changes multiple times, from a game specific web portal called Duowan.com (equivalent of 17173.com of Changyou), to YY Audio (an audio-based IM software), to the latest live streaming.

Li, looks to me, has following attractive traits:

– Strong ethics: based on various interviews, I see Li an ethical manager, who is driven by more than monetary incentives. In his early days as journalist, he is said to be one of few reporters that didn’t reimburse expenses by the tech companies he was covering (which was common practice then). Li also had strong work ethics, confirming by many employees in Zhihu (some combination of Quora and Glassdoor) that Li usually is the last one to leave even when he became CEO.

– Deep awareness of the universe: Li showed strong awareness of psychology & the essence of business model. Li also strongly believed in what he called “end as the beginning” for both product management and live in general, which essentially is the “inverted thinking” model advocated by Charlie Munger.

– Product manager style leader: Similar to Pony Ma of Tencent & Lei Ding of NetEase, Li is said to be fanatic about the details of each product feature.

Li expressed multiple times, in earning calls and interviews, philosophically what live streaming business is to him and how he intends to operate and monetize such a business. Here are some paraphrased quotes:

Live streaming in its most basic form is a community, one that somewhere between stranger and acquaintance. Each community will have its own cognition, culture and value. If a community grows too fast when the original settlers haven’t stabilized, too many new entrants may undermine the culture that bonds the community together and lead to a collapse of the community. Thus a live streaming platform 1) should not acquire traffic by aggressive advertising; and 2) should not try to take all competition.

As an entertainment community, YY is mission is to create and share more happiness to more users. Additionally, YY’s monetization model will mainly base on user’s payment (direct membership fee or indirect virtual items interaction) because it is a more effective monetization model (both for content producers and distributors).

This is a great CNBC interview directly with CEO David Xuelin Li (in English)

System

As YY has a founder CEO, it’s less of concern from interest alignment perspective. Historically, YY also refused to sell to Tencent when they were operating YY Audio. I believe the management has a long term vision in creating value.

Same as for other Chinese company, corporate governance is a major downside. Transparency in corporate communication is also of concern. When I looked back all the earning calls, YY didn’t have any analyst Q&A session in Q2, Q3 & Q4 of 2015 when they experienced major flop in their 100 Education business line.

There is also dilution consideration. Due to the capital requirement for Huya gaming streaming platform expansion, YY already raised two rounds of capital causing some dilution. If Huya is able to pull off a spinoff IPO (rumor says may be listing in HK in early 2018), I don’t think there is capital needs in short term.

Valuation

Sum of part:

YY Live: This piece is relatively easy to value, as the industry enters a maturing stage implying slower growth. However, I believe YY should be able to take more shares during the consolidation phase (reflected in neutral case).

Conservative case: I will just take the 2017 run rate revenue (RMB 8 billion), assume a historical average EBIT margin of 30%, 16% historical average tax rate, 3% inflationary growth rate, & 10% discount rate. and run it off as a terminal value. In this case, YY Live should worth $69 per share. I think these assumptions are extremely conservative, a very small probability event on the negative side.

Neutral case: I will assume YY Live to take more market shares during market consolidation, increasing their market shares to 35~% in a stable TAM (RMB 30b, the lower end) in next two years. Revenue 18E could be RMB 10.5 billion. In this case, YY live should worth around $90 per share alone.

Optimistic case: We can also examine this valuation against a very similar peer MOMO to see whether it’s reasonable. Momo had a very similar transition from a legacy business model (social network) to live streaming. It also shares similar EBIT margin of 30%. However, Momo has a EV/Sales over 5. What it tells me is that Mr. Market think live streaming has no future if looking at YY’s valuation, and thinks completely different if looking at Momo’s valuation. Both views cannot be true at the same time. If we assume he’s right on Momo, YY (taking 2017 run rate of RMB 8 billion) should worth $95 per share alone. If taking my neutral revenue base of RMB 10.5 billion, that’s $125 per share.

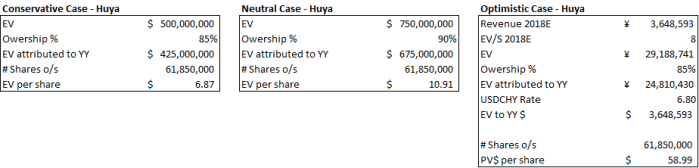

Huya: The gaming streaming platform is not as easy to value as YY Live. It will depend on the TAM materialization and the maturing margin which I have little confidence to predict. A lazy way is probably seeking for historical transaction or comparable.

Conservative/Neutral case: I will just go with their previous round of financing valuation on May 2017. I wasn’t able to find the exact percentage of the business sold for the $75 million round A financing. But I think a 10-15% is a reasonable guess. If assuming 15%, Huya could worth $500 million, and $750 if 10%.

Optimistic case: Not counting on it, but just for fun, let’s see how much Huya could worth when we use Twitch as a comparable. Twitch is a US equivalent gaming streaming platform who got bought by Amazon for $970 million in Aug 2014 (link), and it was reported that Twitch generated about $60 million (link), implying a EV/Sales of 16. Standalone streaming platform won’t justify such a high valuation because of the bandwidth synergy Twitch shares with Amazon’s AWS (I suspect Twitch’s gross margin could be over 75%, and mature EBIT margin over 45% almost like a SaaS platform as they basically have 0 COGS for bandwidth). Even heavily discount the multiple, say to 8, Huya could worth over $59 per share, if you share the same game streaming’s prospects as Bezos.

Net Cash: After the secondary offering in August 2017, assuming all proceeds are still in Cash, YY should have net cash of $863,193 (that is $14 per share). Also note that # of shares outstanding increased to 61.85 million.

In summary:

Why it’s cheap?

– YY had no durable product/service in history

– Unfamiliarity of live streaming business for US centric public market investors

– Concern over the durability of the user-charging business model (US investors favors advertisement monetization model)

However, end of day, all these reasons do NOT explain why Mr. Market see Momo’s model (who suffers all three concerns) differently.

Risk/Bear Cases

- Corporate governance risk

- Regulatory risk

- FX exchange rate risk

Overall, I could not rationalize Mr’ Market’s valuation for YY and see it still has a very attractive risk/reward tradeoff, a position may worth serious portfolio allocation.

Supporting readings (most of them in Chinese)

Meteorology:

http://www.dvbcn.com/2016/09/05-131743.html [2016直播App数据报告] http://www.199it.com/archives/593546.html [易观:2017中国游戏直播市场年度综合分析] http://www.questmobile.com.cn/blog/blog_54.html [QuestMobile网络直播数据] http://www.questmobile.com.cn/blog/blog_67.html [揭秘中国区热门安卓网络直播APP] http://www.199it.com/archives/575027.html [企鹅智酷:2017中国网络视频直播行业趋势报告] http://cn.data.cmcm.com/report/detail/216 [Q3 app ranking] http://cn.data.cmcm.com/report/detail/212 [2017中国泛娱乐社交报告:直播平台、狼人杀和巨头的战争] http://cn.data.cmcm.com/report/detail/209 [复盘:直播的下半场一年,发生了什么?] https://www.zhihu.com/question/38604841 [直播平台review]

Topography:

https://xueqiu.com/5894228201/94853496 [直播风口不再,映客急流勇退] https://36kr.com/p/5100757.html [急流勇退重组公司,映客的命运是创业公司在风口震荡的缩影] https://www.zhihu.com/question/59645876 [宣亚国际为何要收购直播平台映客?] http://www.sohu.com/a/134650485_523234 [看点 | 虎牙YY独占直播版图超半壁江山,映客难再分羹] https://www.toutiao.com/i6485619665648222734/ [2017全网主播上半年总收入全网排行TOP50,YY获得29个席位] http://tech.sina.com.cn/zl/post/detail/i/2016-09-19/pid_8508541.htm [Story of MC天佑] http://www.questmobile.com.cn/blog/blog_93.html [欢乐狼人杀发展势头迅猛,成狼人杀游戏NO.1] https://www.baijingapp.com/article/11863 [李学凌:《Bigo Live》2017 年收入将达 3 亿美元]

Commander:

http://tech.sina.com.cn/i/2017-02-09/doc-ifyameqr7379811.shtml [与马化腾为敌的YY李学凌 最近又要玩出什么新花样] http://www.sohu.com/a/142459296_114795 [李学凌重回CEO位置,代表着YY的革命开始了] https://www.zhihu.com/question/20527479 [李学凌是一个怎样的人?] http://www.sootoo.com/content/672748.shtml [揭秘YY李学凌的社交版图:“以终为始”的他要与马化腾对垒社交] http://finance.sina.com.cn/chuangye/internet/20110805/135710268773.shtml [李学凌:在腾讯的阴影下, very thorough background] http://finance.sina.com.cn/chuangye/internet/20110805/141010268859.shtml [李学凌:我想对马化腾说 http://news.163.com/16/0819/06/BUQF9KK900014SEH.html [YY李学凌卸任CEO放权背后有何玄机?] https://xueqiu.com/5723780667/91245311 [李学凌:以终为始,活得别太当下 |捕手志 good in person interview] http://tech.ifeng.com/a/20170522/44620009_0.shtml [欢聚时代股权曝光:李学凌为大股东 获雷军所持投票权] https://36kr.com/p/5075273.html [YY旗下虎牙直播获7500万美元A轮融资,李学凌重任欢聚时代CEO]

Valuation: Comparable: Twitch, Douyu, Momo

https://www.crunchbase.com/organization/huya-com [Huya Crunchbase] http://www.businessinsider.com/twitchs-investors-win-big-in-amazon-sale-2014-8 [Twitch] https://www.wsj.com/articles/amazon-to-buy-video-site-twitch-for-more-than-1-billion-1408988885 https://www.cnbc.com/2016/05/13/amazons-twitch-streamers-can-make-big-bucks.html https://www.bloomberg.com/news/articles/2017-02-20/chinese-game-site-said-to-seek-funds-at-1-2-billion-valuation [Douyu by Bloomberg] https://www.crunchbase.com/organization/douyutv [Douyu Crunchbase] http://www.iresearch.tv/archives/9973 [Douyu]

Great article. Do you remain bullish on yy? Growth rate of MAU appears to be slowing and the stock has seen a 40% reduction in share price. Can you explain that?

Hi Oluwaseyi,

In addition to the MAU slowing down, market may also dislike the recent regulatory headlines for short videos platforms (Douyin, Kuaishou etc.). No change on my view though, market is really pricing it for decreasing revenue for YY Live (I didn’t factor in any growth for my valuation, except for a mere inflationary kicker), which isn’t materializing. The threat (in competing for the same screen time) from short video is real, however is overestimated by Mr. Market. My view is the tipping streaming users are mostly tipping for the live interaction experience which is not short video is made for. Huya side indeed got diluted by the recent Tencent purchase, which I don’t entirely like… However, the overall effect should be offset at least partially by benefit from Tencent’s backing (branding, traffic & saving on game licensing, etc.)

Thank you for the detailed response. Will huyas financials including user numbers be included in yys financials once huya gets spun off?

Thanks for the article. Have you seen the live streaming industry statistics from the Huya IPO prospectus? The data source there is a Frost & Sullivan report and it looks much more aggressive than your sources. This data applied to 2022 and no growth beyond combined with a higher market share could easily push your neutral scenario above $160 a share. Do you have any thoughts on the Frost and Sullivan data?

Also, at the most recent conference call YY stated that the entrance on the big internet companies into live streaming is net positive for the industry as it would increase people’s awareness and adoption. Do you think the ability of these big companies to direct some of their other product’s traffic to their live streaming poses a real threat for YY or you believe that the YY community sense and hence, their users base and growth would remain intact?

Your feedback will be much appreciated.

Hi Aleks, I missed your comment, sorry about that. My reply may not be as relevant now, but to your point:

– HUYA f1: certainly rosy assumption, but not impossible. Huya was a big piece margin of safety in my original thesis. The Tencent deal certainly took a big bite out of it at a ludicrous low price…

– I’m still comfortable with its competitiveness in entertainment streaming vertical. It’s been tested in Inke’s case. IMO, in addition to deep pocket & traffic, you need some “cult” ingredient (a key for monetization) to overthrow YY’s leading position, which is very hard to come by. Douyin these days certainly has it, would be interesting to see how they monetize it.

Thank you for the thoughtful thesis. It was a great read – what’s your view on fad risk and hence terminal value risk of live streaming platforms as a whole? I.e. how do you get comfortable that user engagement will not fall off a cliff given the highly discretionary nature of tipping spend, concentrated paying user base (majority of MAUs don’t pay), continued emergence of new entertainment options?

Would love to hear your perspectives. Thanks!

Thanks for the nice words, Jerry. I think you do need to make a subjective judgement call on whether it’s fad or here to stay, which is the main reason for the mispricing I’m seeing based on my judgement. I believe this form of interactive entertainment meets some psychological needs that I don’t have a good word to describe (almost like the a virtual life). But for core users, I believe the tipping is deeply embedded in their subconsciousness that they do deem it as indispensable. It’s not hard to find reports on people try to live in austerity or even to steal, to support their streaming virtual life. Not healthy individual choices, but the point is to judge whether these spending are “discretionary”.

As for new options, it’s always a risk. that’s why you need to get comfortable with their management’s ability in steering innovation and strategic choices. IMO, they are not bad in innovation, strategy and execution. But not good corporate governance though (as showed in the recent HUYA sell).

Concentrated paying user base, in the context of last risk, is a good thing IMO. That means its success is not reply on growing (or maintaining) MAU, rather on cultivating and keeping core users. In other words, it can risk losing users to new options to a certain degree.

End of day, it is the price that I get comfortable with (after incorporating all risks), not the risks themselves. So this is not some “sit on my ass” position, but something I need actively reassess regularly.

Hey Tao Value,

How do you feel about YY Inc sharing a bigger portion of their revenue with the content producers (streamers)? I’d think the entire moat of YY lies with the content producers and YY’s platform is not as sticky as it seemed to be. Would it be unsustainable?

Not sure if I understand your first question, IMO, it is the content producers share revenue with YY (the users consume content and pay the producer through a distribution platform, and the platform in this case take a cut of the payment)… not the other around.

If you look long enough, nothing is “sticky”. Any biz model will be disrupted. The question here is for “how long” it can remain sticky, and is the company keep innovating to keep it sticky. This is the key question market has different view than me, obviously. Narrative about sustainability of streaming has come up since 2016, but I don’t see their top line falls off the cliff as many have predicted. A legit concern is saturation of growth in mainland China, where you don’t have new mobile internet users and fierce competition of other types of entertainment options (Douyin etc.). So I would expect they may have margin squeeze (more S&M expense for keeping users), but I don’t worry about their top line as much (my valuation assume stalled top line). That’s also why I think buying Bigo to tap overseas streaming market is a wise move.

Certainly could be wrong, but that’s my latest assessment. Welcome your feedback. Thanks.

Thanks for all your comments,

I read this article on CNBC today and it paints a pretty dire picture for the future of the live streaming business: https://www.cnbc.com/2018/09/19/short-video-apps-like-douyin-tiktok-are-dominating-chinese-screens.html

What are your thoughts?

For a moment I thought may be I should cut my losses but then I looked at the valuation and this business net of cash and the Huya stake is trading as if there is one or max two more years left before it is all over which is a bit too conservative I feel.

Do you think the facts (mainly around short form competion) have changed materially since you wrote this article so much so a re-evaluation of the thesis is granted?

Regards,

Aleks

Hey Aleks,

YY’s been my biggest loss (unrealized) this year, however I’m fine keeping holding it at my size (you should judge from your perspective what is a right position size given your conviction of the idea). Live streaming will become obsolete someday (like any business), but I don’t think it will be for short videos. I don’t think the end will be here soon either. In fact, the more I study live streaming, the higher I think of this business model. It is probably one of the most effective monetization model of “influence”, where the influencees were put in a continuous auction session for influencer’s live interaction.

– Yes, MAU is slowing down by these mentioned competition. However how relevant MAU growth is for a well established business model monetizing on a very concentrated user base subset? Why YY’s revenue can keep growing (albeit at slower pace)? If I could, I only want to learn the metrics for the 20% high spending users who probably contributed 80% of the revenue. YY unfortunately don’t disclose that.

– Yes, YY is down a lot, but how much are attributed to YY’s specific business value deterioration? or alternatively how much more Mr. Market know about YY specifically than broader EM fear? If you look at YY’s correlation to CQQQ (a Chinese Tech ETF only had 2.6% holding in YY) over past a few months, it’s well over 90%. It looks to me the price drop could be explained mostly by a broad fear to Chinese tech companies as a whole (or the trade war as a whole).

– Back to short video, a few observations I have are 1) many famous streaming hosts do have Douyin account, however they still do live streaming actively on YY (why? because at YY they can monetize their influence most effectively) 2) one professional singer is moving to YY (that means YY’s monetization is even more effective than some of the traditional profession performer model). I see short videos are more like CDs of the old days, would you stop going to live concert of your favorite singer just because you had his/her CD album? No, in fact new medias like short video may help the performers to spread their influence to more audiences, and could even be a good thing for YY. As far I observed, short video platforms are going down the ad revenue model, so I don’t think it would affect YY’s model too much.

The real threat to YY is always a more effective monetization model of influence, for which I’m still keep out looking for but haven’t identified it yet.

Thanks, I appreciate your very valid points. That helps me get more comfortable with the live streaming side of the business as the main reason I invested in YY was to get a cheaper exposure to the Huya business (similar to getting exposure to Weibo through SINA) and as long as the live streaming did not fall off a cliff I thought the stock should do pretty well being pulled forward by the game streaming. Clearly, trying to be too smart has not worked for me so far but I also agree that had we no had the US-China trade skirmish YY would have traded significantly higher. Ultimately, if the next few conference calls reveal that the live streaming business countinues to maintain its profitability (not even grow) the stock should return back to more reasonable levels (towards the 100s).

Regards,

Aleks

Amazing post. Thanks a lot for sharing your deep knowledge about the company and the sector.