Coty is a new position last quarter. As mentioned in my Q3 letter, I think the “system” factor of Coty is very impressive. As an effort to document my own learning as well as knowledge sharing, I here formalize my notes. It’s not intended as a support for my judgement, rather I think it would be beneficial in general for anyone who involves in a principal-agent situation (e.g. board of directors, entrepreneurs, etc.) for designing or assessing incentive systems.

Investing community generally agree that a management with owner mindset is preferred. But how exactly could one evaluate “owner mindset”? One way is to talk to the management in person and make assessment qualitatively, however that’s not possible for all shareholders. CEOs typically are also very good at marketing themselves, which adds another layer of uncertainty. These are the reasons why some investors prefer founder CEOs, who are inherently owners.

Coty’s incentive system has following uncommon designs based on a heavy ownership philosophy.

1) 5-year cliff vesting: this means the agent will get nothing until 5 full years after the grant. A more common vesting schedule is straight line vesting (each year vesting 1/n of the grant for n years). Cliff vesting ensures the agent will try to adopt as long-term perspective as possible, meanwhile also ensure key executive retention. By and large, the more deferred, the better.

– Source: Coty 2016 Proxy Statement

2) Matching RSU/options/preferred if management makes open market purchases. This mechanism essentially encourages management to actively express their view when they think stock price is undervalued. After all, if the management had no faith in the company, any additional benefit from RSU, preferred or options would be wiped out by the loss incurred in their bought stock position.

– Source: Coty 2016 Proxy Statement

3) Management has $value minimal holding guideline: Although the proxy statement didn’t indicate whether the guideline is mandatory, it is safe to assume management would meet it voluntarily even just to be looked good in front of board. Coty, in this case, requires CEO to hold 5* base salary and other executives 3* base. This means management would have to pay directly out of their pocket to maintain the $ holding if price slides significantly. I like it a lot because even part of management’s holding is granted over time through equity based comp, the pay-out could create extra pain (which they will try their best to avoid).

– Source: Coty 2016 Proxy Statement

Additionally, there is also downside incentive (i.e. punishment) for not meeting this guideline. For the options/preferred matching program, management needs to maintain this holding level.

– Source: Coty 2016 Proxy Statement

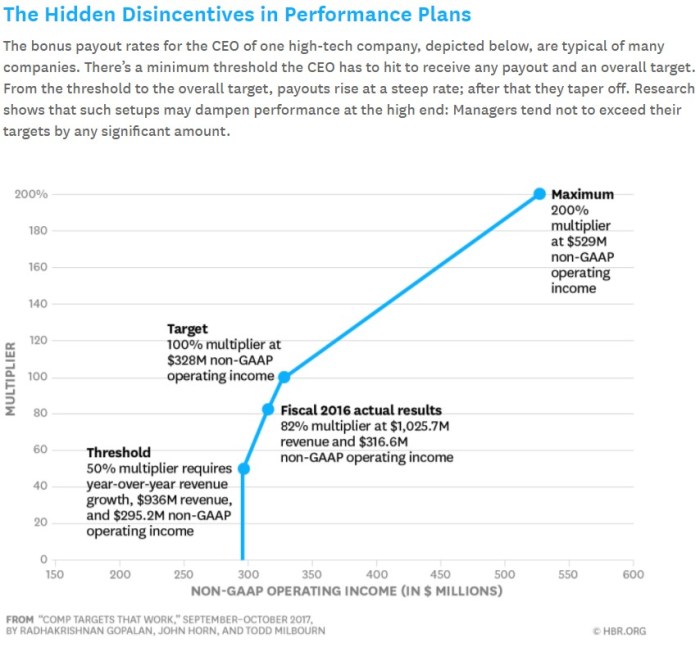

4) Convex performance target curve: This part will require some background reading. A recent Harvard Business Review piece (Link) examined the effectiveness of compensation target setting for executive managers and had some interesting findings. One of them shows a concave performance target curve would encourage management to meet the target, however dampening the possibility of outperforming, as showed in below chart.

– Source: HBR.ORG

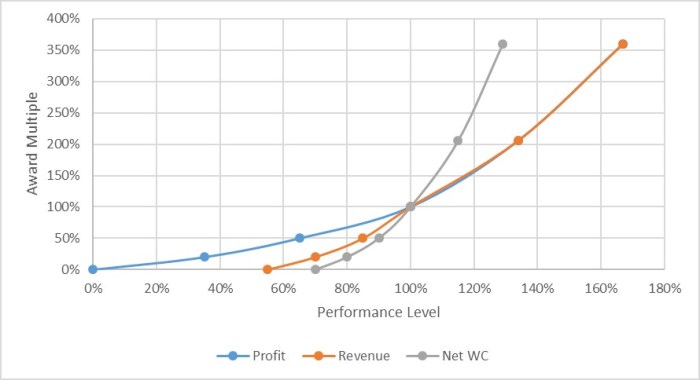

For Coty, we however see a convex curve. Although it is not straight line as suggested by the research, I see it is more favorable for incentivizing outperformance. In other words, if the management realize the outperformance is more achievable, they would more inclined to hit it.

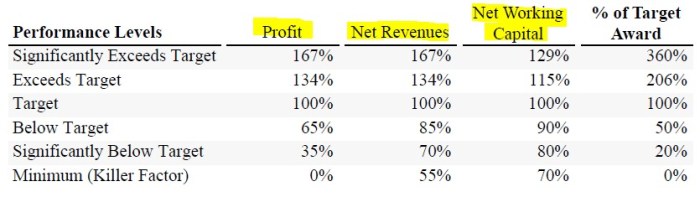

5) Key metrics used in the comp target. Generally, company would use revenue which is a good start (less possibly to be manipulated). When it comes to earning/profit, different companies use very different measures and in most of case it is not GAAP/IFRS earning. The reason is to reflect the true economic profit creation. A key requirement for investors here is to evaluate whether these non-GAAP adjustments make economic sense. (still remember the “adjusted cash flow” from Valeant?)

In Coty’s case, they chose below three – Profit (adjusted earning), Net Revenues & Net Working Capital. No wonder Coty’s CFO, Patrice de Talhouët, couldn’t stop highlighting their negative net working capital in their Q4 2016 call. This shows how effective the incentive system work – using self-interest to direct agents to follow guideline set by principals.

6) Peer selection: This is a typical practice, where management’s performance will be “curved” by the peers. One should double check this list includes all the relevant (and preferably the best) players in the same space. For Coty, it is good that they have L’Oreal and Estee Lauder, two best beauty products companies, in this list.

Going back to Coty as a investment, there shouldn’t be doubt that Coty is a troubled business, especially in its Consumer line. However, I sense that Mr. Market may have discounted its very well-orchestrated incentive system (or didn’t take it into consideration at all). Although I admit incentive has very little predictability for short term return, this finding changed my evaluation of the probability of long term favorable outcome driven by motivated management. One way or another, participation of such situation should benefit me. Head I make money, tail I learn a lesson.