Below is my letter for 2021 Q4. I looked back to our first 5 years and looked forward on where the Market may go.

Author: taovalue

Investor Letter – 2021 Q3

Below is my letter for 2021 Q3, in which I shared my thoughts on the issue of Facebook and of social platforms as a whole. I also discussed extensively about our new position – Roblox (RBLX).

Thoughts on China’s Regulatory Landscape

Below is the market commentary excerpt from our recent 2021 Q2 letter.

The Rise of Mr. Government

Modern finance, as a school, was developed by western civilization. Investing, as a derivative of finance, can be said the same. Among all the value investing books published, there are very few mentions of evaluating government as a stakeholder or risk associated. This is unsurprising because the whole western economy system is built upon free market economy theory which believes government should intervene as little as possible. When capitalism grows more mature, we started to see a reversal shift from such premise, most recently in Big Tech regulation, but that is nowhere close to the role Chinese government plays in its economy. This is why I stressed heavily on value creation for all stakeholders, including the government, in my framework.

In the past quarter, we have seen humbling evidence of how important Mr. Government is to Chinese businesses, as waves of looming regulations on Chinese businesses materialized. E.g. the new law curbing private education was released in May. It explicitly stresses the non-for-profit nature of K9 schools and strictly prohibits related party transaction to move the profits out and M&A of schools. In July, the Cyberspace Administration of China launched data-security investigation on a few newly IPO’d Chinese tech firms, most prominently Didi, the ride hailing dominator in China. As I’m writing this letter, government delivered another heavy blow to after-school tutoring industry by releasing the Opinions on “Double Reduction” for Students in the Compulsory Education Stage, which essentially ruled all subject-related tutoring should be non-profit. Against such backdrop, some Chinese stocks suffered panic selling in similar scale only seen in 2008 financial crisis.

Implications on Investors’ Trust

Many called such interventions “unconstitutional”, “confiscation” or “authoritarian”, and starts to claim that Chinese stocks are not investable at all. I don’t fully agree with such view. For private education, I was supportive for certain tighten-up by stating “Without a sound regulatory framework, such a market is destined to be flooded by greedy and predatory players” in my last letter. Chinese government & economy, in my opinion, is a very complex hybrid system with its own merits. It seems to me that most western observers do not understand it and tend to use century-old ideology to over-simplify it. Taking one recent example, Charlie Munger in his interview with CNBC on June 29th, 2021, touched on Chinese regulation, crediting China by saying “…a wise regulator stops this stuff [Archegos’ meltdown] before it starts…what interests me in this is that the communist Chinese behave the way I am talking in favor of”. Such response disturbed even many value investors who are known for following Buffett & Munger as a cult. It seems to me that such misunderstanding is widespread and now exacerbated by the political tension between US & China. Without a deep understanding of how China works, foreign shareholders won’t be able to hold through turmoil like this one.

Widely in western investing frameworks, there are generally two pillars: fundamentals (related to the company) & valuation (related to Mr. Market). For a sound framework for future investing, I believe a third pillar of same significance on regulation (related to Mr. Government) should be added. Before this point is fully ingested by global investors, Chinese companies listed overseas may lose confidence in general and may carry lower valuation than global peers.

Our Understanding of the China Model

Helped by a hybrid model of socialism & capitalism, China, with over 1 billion population, grew its GPD per capita from $195 in 1980 to $10,262 in 2019. (i.e., a 52 folds jump or 11% annualized growth over a 39 years period!) Yet, critiques claim that this model is not based on a plural political system and that it is authoritarian. It is fair to say that the top priority of Chinese Communist Party (CCP) has always been maintain its power, which is true for any political party. What’s unique about the China model, however, is that CCP desperately tries to justify the legality of its power in a practical way – that it must be earned by improved welfare of the whole society.

Without the Separation of Powers, Chinese public administrative system serves legislative & executive roles at the same time. A typical process runs like this: 1) Central government drafts, solicits feedbacks & finalizes guidance documents. Such documents are conceptual and brief in nature; then 2) Individual agencies or Local governments use discretion to interpret the guidance, to design detailed policies & to enforce the implementation.

Such unified power, while with good intention, can utilize the best parts from socialism & capitalism and can be very effective and flexible. Take one example from not far ago, China started promoting Electric Vehicle (EV) around 2010. The market was initially swamped by players who built “cars” that better to be described as toys, only to cheat for subsidies. Over time, the government iterate through few versions of regulation, e.g. using technical specs like range to scale subsidy. Nowadays, China has multiple EV brands that can compete locally at the same level with market leading Tesla. Some of the EV technology developed by local EV companies like BYD are also recognized by global auto manufactures like Toyota in form of partnership.

After observing generations of such policies, I think the China model typically overshoots at the initial stage with little fear of making mistake (e.g. over-promoting if it intends to promote; & over-curbing if it intends to curb), but is generally fast in iterating and finetuning towards the conceptual goal identified by the central government.

Investor Letter – 2021 Q2

Below is my letter for 2021 Q2, in which I shared my thoughts on Chinese political & economic system, and its implication on regulatory impact on our portfolio companies.

Investor Letter – 2021 Q1

Below is my letter for 2021 Q1, in which I shared my thoughts concerning Chinese education businesses and commented on new positions of Tianli Education (1773.HK), TAL Education (TAL) & Futu Holdings (FUTU).

The Great “Retailization” of US Market

It is an short excerpt from my 2020 Q4 letter [Link], but it felt like long time a ago since the GameStop story folds out. I think this new phenomenon may have profound impact to the market structure. For example, how do we define a “right” price, and what is “market manipulation” exactly? Historically, price manipulation happened when few entities comer the market and set price by transacting between colluded parties. In that way, such price is not “right” because it’s not agreed by a widely participated market (i.e. an authoritarian price). If the “right” price is defined as the price agreed by majority in a widely participated market (i.e. a democratic price), isn’t the currently price of GameStop (closed at $347.51 on 1/27/2021) a “right” price? and if it’s a “right” price, where is the “manipulation”?

One hallmark of US equity market in 2020 is what I called the great “Retailization”, where the asset pricing function seemed to heavily shift to the hands of retail investors. Lately, I was able to get hands on a proprietary dataset which confirmed this phenomenon. On left chart below, you can see the retail trades in % of total equity market trades held at a level of 12% from 2017 to early 2020, then jumped up to a level of 25% in late 2020.

Additionally, retail is not “dumb” money anymore! At least judging from short term return perspective. On the right-hand side chart below, you can see a hypothetical one day holding period L/S strategy to buy the 10% most bought stocks by retail investors on that day and short the 10% most sold stocks at the close and exit positions at the next close. The most obvious thing you would notice is the clear infection point in March 2020 when US shut down for the pandemic. Even before that, this signal still predicts positive one day forward return (i.e., the prices follow what retail investors flow), yet in a milder form (13~% annualized return). Since March 2020, such signal started to show stellar predictive power, leading to a 97% annualized return! This is a solid confirmation, using data, that Mr. Market now is basically a retail trader.

Now that we see the “what”, it is important to think about the “why” (it happened), and the “how” (to prepare for it). There is more retail participation as the market share analysis shows, but there is still 75~% of institutional flow. However, if we try to break it further down by active & passive flow, and assuming passive institutional flow are not pricing assets, we can argue retail now has a much stronger hand against active institutional flow, especially in certain sector (e.g. tech), or certain stocks (e.g. Tesla).

Looking forward, I start to think about the implication, here are what could happen (or may already be happening):

- The rise of a new breed of investor, who make “profiting in stock market” seemingly easy.

- The rise of star fund managers using new paradigms.

- Capital Market are transformed by an influx of new personnel who only had experience of a prolonged bull market.

In case you have not noticed, I just copied some description for the Nifty Fifty bubble in 60s to 70s. The parallel between now and then seems obvious, yet I think there are a few nuances in today’s market: 1) I believe businesses today have a sounder fundamental, which probably only seen in the last Industry Revolution; & 2) The speed of information is exponentially faster than in the 70s. This leads to me to think that we may be at the beginning of a larger “bubble” than Nifty Fifty, yet in a faster pace. I think that new paradigms today have their merits but will very possibly be pushed to extreme by elevated retail participation. One key lesson from Nifty Fifty era is that valuation still matters even though one can do fine in long term if holding great businesses through a huge bubble.

Investor Letter – 2020 Q4

Below is my letter for 2020 Q4, in which I commented on new position of Yihai (1579.HK), PLTR & GBTC. I also shared my analysis & thoughts on the “Retailization” of the market.

pdf below:

In Search of Mindful Compounders

Note: It’s a republish of the General & Market Commentary section of 2020 Q3 Letter, for easier reference and access.

This pursuit started from studying my own largest omission mistakes (i.e. failed to buy the companies when I could have), namely Amazon, Microsoft (post Satya Nadella), Netflix. But before we dive in, I need to clarify what “mindful compounder” means. I see “compounder” as who persistently create value (not monetary value alone) for all stakeholders across the value chain, and “mindful” is a generalization of many traits I look for Tao & Commander factor, e.g. mission driven, purposeful, rationality, deep thinking & high awareness. (see more in my investment process post[1]). In all cases, I have identified the managers of these companies as mindful leaders yet didn’t buy for the fear of market being already efficient in pricing these mega cap stocks.

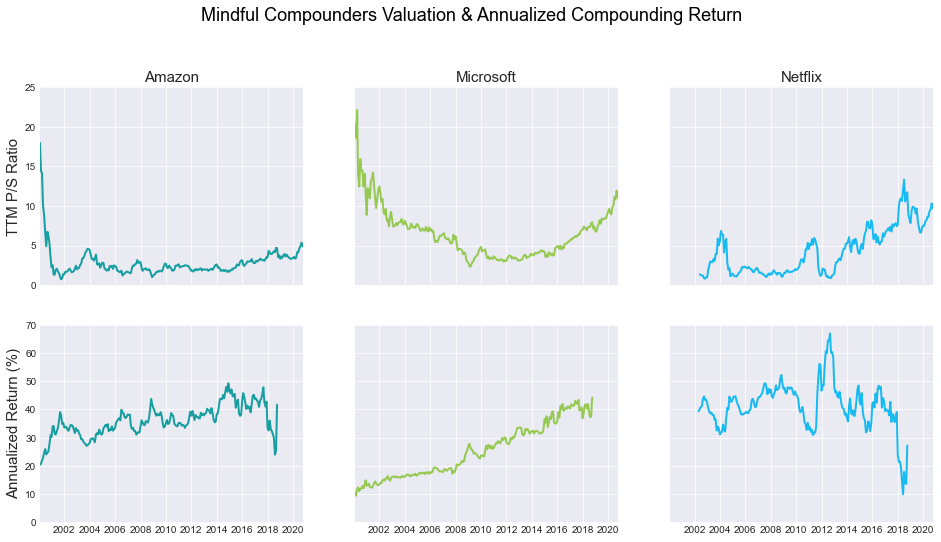

But how efficient has Mr. Market been in pricing the value of these companies really? Below I draw the time series of valuation (TTM P/S ratio), and annualized compounding return to date (i.e. if holding form that point of time to 9/30/2020). I excluded annualized return for recent 2 years since they are not representative for the short history.

One clear lesson to be learn here is that market has been far from efficient in evaluating the intrinsic value of these companies. Taking Amazon for example, the worst time to buy it was in January 2000 when it was priced at 17 P/S ratio, but you would still achieve 20+% annual compounding return if you hold till now. Buying it any other time later than 2004 and hold it till now would give well above 30% annual return! Obviously, valuation still matters, but the worst scenario of 20% is far cry from an efficient market return over 20 years. So, the market must have missed something! Luckily, all three companies have long history for me to study patterns that can help identify value earlier.

The “Stumbled-Upon” Quantum Leaps

The first important pattern is that none of them relied on a single product/service to achieve the substantial value compounding. As old businesses mature, all these companies in their lives experienced some pivotal “quantum leaps” expanding to new products/services, which ultimately contribute heavily to its long-term value but was not fully appreciated by the time. With few exceptions, the leaders later would admit that the leap was not by design, or at least that they didn’t foresee the full potential. For example, Netflix had two major pivots from DVD renting, to streaming & to original content. Microsoft also made a major pivot after Nadella took the helm to “cloud & open source first”. Amazon’s AWS was an internal tool built out of its own frustration of its ability to launch new projects/applications, later became a $40 billion annual run rate revenue monster!

Surrogation Bias & First Principle

All companies try to “leap” too, but more often they end with disappointment. I think what makes mentioned 3 compounders more successful in making such leaps is their mindfulness. Case studies of the failed attempts point to a pervasive, yet understudied bias – Surrogation, whereby the measure of a construct of interest evolve to replace the construct itself. Take Wells Fargo’s fake account scandal as example[2], the management initially use cross selling metrics to measure its relationship with clients. However overtime, subsequent executives started to believe the cross selling is the strategical goal (rather than client relationships), leading to the now-infamous mantra – “Eight is great” (to have 8 Wells Fargo products per customer). What made things worse is management started to tie incentives to this single metric for front line bankers, which ultimately led to faking accounts. Such misalignment is detrimental for company value.

On the other hand, all three mentioned companies deeply embed first principle in their operation to overcome surrogation. Amazon provides probably the best example, from Bezos’ first shareholder letter, Amazon has been obsessively following a “customer-centric” philosophy and repeatedly use this qualitative principle to guide quantitative measures & decision making. For example, Amazon started very early to not only use GMV & MAU to define their performance, but also added repeating customer orders because it was a better way to measure the stickiness, or value created for customers. Pinduoduo (one of our current holdings) is another example in putting a qualitative Polaris for Social E-Commerce (To focus on user engagement) around any measurements. Chairman Colin Huang in many occasions dismissed sell side analysts’ question regarding its ARPU trend & guidance saying:

… raising ARPU is not part of our management’s KPI, but I think it will be a natural result as the users’ engagement increases over time…

– Colin Huang, PDD 2020 Q1 Earnings Call

Also, regarding the measurement of users’ engagement, it uses a unique and well-thought-through metric – MAU/Annual Active Buyers. It is like Amazon’s idea of repeating customers orders, but more consistent in a normalized % form.

Radical & Prescient Decision Making

Another common theme I observed from mentioned companies is that on top of the first principle thinking, management tend to make seemingly radical decisions later proven prescient. Microsoft’s Satya Nadella made an impressive example[3], especially considering his soft-speaking personality (e.g. he’s never seen “upset, raising voices or firing off angry email” by colleagues). Yet he demonstrated assertion in many big decisions even early in his tenure as CEO. For example, Nadella decided to write off $7.6 billion from Nokia purchase first year in 2015 and to terminate its Windows division, which was split into Azure & Office divisions in 2016. Additionally, during the agonizing Windows to Azure reorganization (which one executive called “pulling fingernails”), Nadella showed his exceptional ability to make aggressive changes with little drama.

Netflix’s Reed Hastings, a half-mentor of Nadella (as board of Microsoft), is a hallmark of such decision-making ability[4]. Although the decision of pivoting to streaming & original content are both monumental, I think the most radical & prescient decision may be the one he made in earlier year to call off its streaming hardware right before its launch. I was December 2007 and Netflix has been exploring variety of new business models as its legacy DVD renting line matures. A team of about 20 had been working around the clock for years on a project coded “Griffin”. It was so close to the launch that marketing materials had been printed, advertisements were being shot, and Foxconn, the manufacturing partner, was ready to kick off production. Yet to the surprise of all the insiders, Hastings decided to kill it (subsequently it was spun off and became Roku). The magnitude of this decision is now much more clear, had Hastings chosen to pivot to the hardware business, they would compete with all other hardware players (TVs, Apple etc.) and wouldn’t be able to consolidate the demand side which is a conner stone of its later licensing streaming flying wheel. Roku, even at today’s steep valuation, would be worth 1/10 of the current Netflix. According to one inside source, Hastings explained this hard decision in a very simple but vivid way:

“I want to be able to call Steve Jobs and talk to him about putting Netflix on Apple TV, but if I’m making my own hardware, Steve’s not going to take my call.”

[1] Tao Value Investment Process: https://taovalue.net/2017/07/17/sun-tzus-five-factors-business-analysis-framework/

[2] Don’t Let Metrics Undermine Your Business, Harvard Business Review, https://hbr.org/2019/09/dont-let-metrics-undermine-your-business

[3] The Most Valuable Company (for Now) Is Having a Nadellaissance https://www.bloomberg.com/news/features/2019-05-02/satya-nadella-remade-microsoft-as-world-s-most-valuable-company

[4] Inside Netflix’s Project Griffin: The Forgotten History Of Roku Under Reed Hastings https://www.fastcompany.com/3004709/inside-netflixs-project-griffin-forgotten-history-roku-under-reed-hastings

Investor Letter – 2020 Q3

Below is my letter for 2020 Q3, in which I commented on new position of BEKE, WORK, & API. I also shared the case studies of why focusing on “mindful compounders” is important.

pdf below:

Investor Letter – 2020 Q2

Below is my letter for 2020 Q2, in which I commented on individual holdings of PDD, YY, AVLR & CIH. I also shared my process of evaluating opportunity cost of trading actions, and how it improves learning from own past successes, misses & biases.

pdf below: