Note: It’s a republish of the General & Market Commentary section of 2020 Q3 Letter, for easier reference and access.

This pursuit started from studying my own largest omission mistakes (i.e. failed to buy the companies when I could have), namely Amazon, Microsoft (post Satya Nadella), Netflix. But before we dive in, I need to clarify what “mindful compounder” means. I see “compounder” as who persistently create value (not monetary value alone) for all stakeholders across the value chain, and “mindful” is a generalization of many traits I look for Tao & Commander factor, e.g. mission driven, purposeful, rationality, deep thinking & high awareness. (see more in my investment process post[1]). In all cases, I have identified the managers of these companies as mindful leaders yet didn’t buy for the fear of market being already efficient in pricing these mega cap stocks.

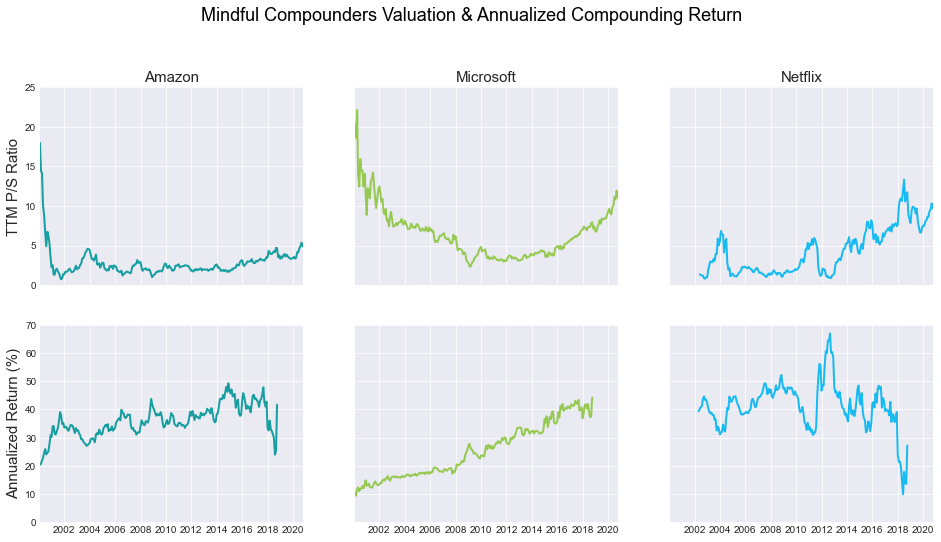

But how efficient has Mr. Market been in pricing the value of these companies really? Below I draw the time series of valuation (TTM P/S ratio), and annualized compounding return to date (i.e. if holding form that point of time to 9/30/2020). I excluded annualized return for recent 2 years since they are not representative for the short history.

One clear lesson to be learn here is that market has been far from efficient in evaluating the intrinsic value of these companies. Taking Amazon for example, the worst time to buy it was in January 2000 when it was priced at 17 P/S ratio, but you would still achieve 20+% annual compounding return if you hold till now. Buying it any other time later than 2004 and hold it till now would give well above 30% annual return! Obviously, valuation still matters, but the worst scenario of 20% is far cry from an efficient market return over 20 years. So, the market must have missed something! Luckily, all three companies have long history for me to study patterns that can help identify value earlier.

The “Stumbled-Upon” Quantum Leaps

The first important pattern is that none of them relied on a single product/service to achieve the substantial value compounding. As old businesses mature, all these companies in their lives experienced some pivotal “quantum leaps” expanding to new products/services, which ultimately contribute heavily to its long-term value but was not fully appreciated by the time. With few exceptions, the leaders later would admit that the leap was not by design, or at least that they didn’t foresee the full potential. For example, Netflix had two major pivots from DVD renting, to streaming & to original content. Microsoft also made a major pivot after Nadella took the helm to “cloud & open source first”. Amazon’s AWS was an internal tool built out of its own frustration of its ability to launch new projects/applications, later became a $40 billion annual run rate revenue monster!

Surrogation Bias & First Principle

All companies try to “leap” too, but more often they end with disappointment. I think what makes mentioned 3 compounders more successful in making such leaps is their mindfulness. Case studies of the failed attempts point to a pervasive, yet understudied bias – Surrogation, whereby the measure of a construct of interest evolve to replace the construct itself. Take Wells Fargo’s fake account scandal as example[2], the management initially use cross selling metrics to measure its relationship with clients. However overtime, subsequent executives started to believe the cross selling is the strategical goal (rather than client relationships), leading to the now-infamous mantra – “Eight is great” (to have 8 Wells Fargo products per customer). What made things worse is management started to tie incentives to this single metric for front line bankers, which ultimately led to faking accounts. Such misalignment is detrimental for company value.

On the other hand, all three mentioned companies deeply embed first principle in their operation to overcome surrogation. Amazon provides probably the best example, from Bezos’ first shareholder letter, Amazon has been obsessively following a “customer-centric” philosophy and repeatedly use this qualitative principle to guide quantitative measures & decision making. For example, Amazon started very early to not only use GMV & MAU to define their performance, but also added repeating customer orders because it was a better way to measure the stickiness, or value created for customers. Pinduoduo (one of our current holdings) is another example in putting a qualitative Polaris for Social E-Commerce (To focus on user engagement) around any measurements. Chairman Colin Huang in many occasions dismissed sell side analysts’ question regarding its ARPU trend & guidance saying:

… raising ARPU is not part of our management’s KPI, but I think it will be a natural result as the users’ engagement increases over time…

– Colin Huang, PDD 2020 Q1 Earnings Call

Also, regarding the measurement of users’ engagement, it uses a unique and well-thought-through metric – MAU/Annual Active Buyers. It is like Amazon’s idea of repeating customers orders, but more consistent in a normalized % form.

Radical & Prescient Decision Making

Another common theme I observed from mentioned companies is that on top of the first principle thinking, management tend to make seemingly radical decisions later proven prescient. Microsoft’s Satya Nadella made an impressive example[3], especially considering his soft-speaking personality (e.g. he’s never seen “upset, raising voices or firing off angry email” by colleagues). Yet he demonstrated assertion in many big decisions even early in his tenure as CEO. For example, Nadella decided to write off $7.6 billion from Nokia purchase first year in 2015 and to terminate its Windows division, which was split into Azure & Office divisions in 2016. Additionally, during the agonizing Windows to Azure reorganization (which one executive called “pulling fingernails”), Nadella showed his exceptional ability to make aggressive changes with little drama.

Netflix’s Reed Hastings, a half-mentor of Nadella (as board of Microsoft), is a hallmark of such decision-making ability[4]. Although the decision of pivoting to streaming & original content are both monumental, I think the most radical & prescient decision may be the one he made in earlier year to call off its streaming hardware right before its launch. I was December 2007 and Netflix has been exploring variety of new business models as its legacy DVD renting line matures. A team of about 20 had been working around the clock for years on a project coded “Griffin”. It was so close to the launch that marketing materials had been printed, advertisements were being shot, and Foxconn, the manufacturing partner, was ready to kick off production. Yet to the surprise of all the insiders, Hastings decided to kill it (subsequently it was spun off and became Roku). The magnitude of this decision is now much more clear, had Hastings chosen to pivot to the hardware business, they would compete with all other hardware players (TVs, Apple etc.) and wouldn’t be able to consolidate the demand side which is a conner stone of its later licensing streaming flying wheel. Roku, even at today’s steep valuation, would be worth 1/10 of the current Netflix. According to one inside source, Hastings explained this hard decision in a very simple but vivid way:

“I want to be able to call Steve Jobs and talk to him about putting Netflix on Apple TV, but if I’m making my own hardware, Steve’s not going to take my call.”

[1] Tao Value Investment Process: https://taovalue.net/2017/07/17/sun-tzus-five-factors-business-analysis-framework/

[2] Don’t Let Metrics Undermine Your Business, Harvard Business Review, https://hbr.org/2019/09/dont-let-metrics-undermine-your-business

[3] The Most Valuable Company (for Now) Is Having a Nadellaissance https://www.bloomberg.com/news/features/2019-05-02/satya-nadella-remade-microsoft-as-world-s-most-valuable-company

[4] Inside Netflix’s Project Griffin: The Forgotten History Of Roku Under Reed Hastings https://www.fastcompany.com/3004709/inside-netflixs-project-griffin-forgotten-history-roku-under-reed-hastings