On 5/22/2017, Changyou [CYOU] received a preliminary non-binding offer from its chairman Dr. Charles Zhang, who is also the CEO and Chairman of Changyou’s parent company Sohu, to take the company private with and offer of $42.10 per ADS. The offer letter can be seen here: http://ir.changyou.com/05_22_2017.shtml. It is interesting that it is Charles Zhang, the person, not the parent company Sohu, to make the acquisition.

As a current CYOU shareholder, I think it’s a OK deal despite I had higher expectation of the turnaround execution which just started to show some positive signs. As of 5/31/2017, there is still about 8% spread between the close price of $38.9 and offer price $42.1. If the deal could be closed timely, it would be a good risk arbitrage opportunity.

Inspired by this event, below I did a general study of all the Chinese ADR “go-private” deals in past few years. I’m keen to get answers to these 3 questions (which could help me evaluate upcoming similar deals’ risk/reward):

- How much percent of these deals fell through?

- What are the characteristics of the failed deals? (does CYOU have any of these traits?)

- How long do they usually take to close?

History of Chinese ADR Privatization Deals

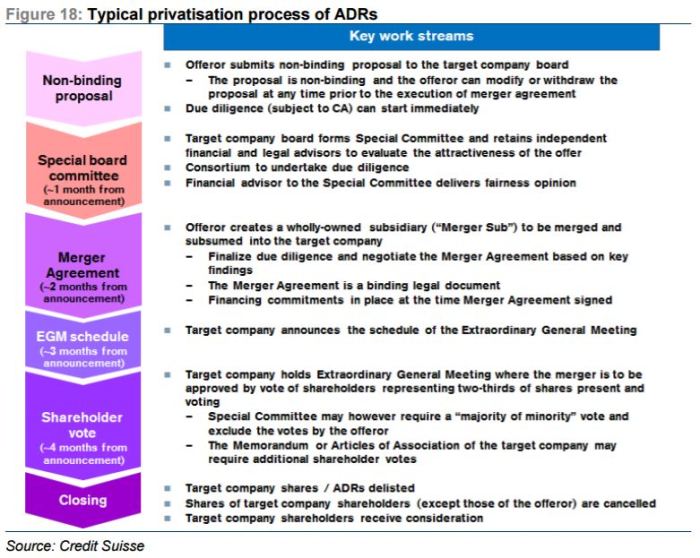

Let’s begin with a rough understanding of a typical ADR privatization process. Credit to a Credit Suisse’s study [link here], here is a great chart showing the 6 milestones of such a process.

It is also important to understand the main incentive of such privatization deals, specifically for these US listed Chinese companies. Like most of the PE backed LBO deals, Chinese ADR privatization deals also target for a relist for higher valuation. However the difference is that, rather than streamlining and growing the businesses for a few year in private arms (in LBO cases), the Chinese ADR companies could seek a faster re-valuation by relisting the firm to its home market (which offered richer valuation, especially back in 2015 before the crash). This also explained why there were so many proposed deals announced in 2015.

Probability of the Deals

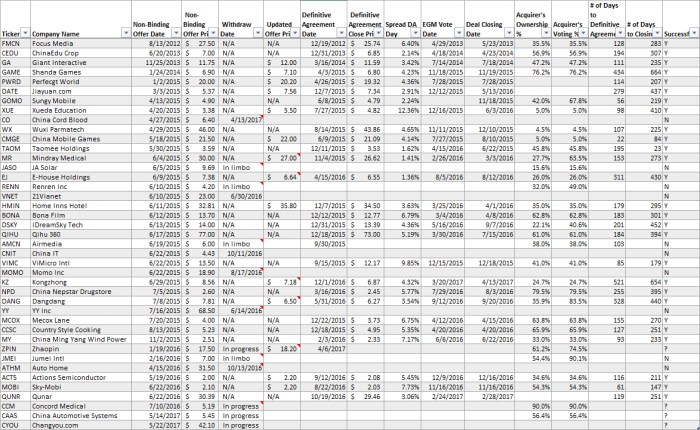

I compiled a list of 41 announced Chinese ADR “go-private” deals from 2012 to date (completeness not guaranteed). Below is a screenshots of the key data points I collected. In addition to the dates of milestone events, I add a few more metrics that I deem important to evaluate the possibility of the deal going through: 1) Whether the deal is CEO/Chairman led; 2) Acquirer’s consolidated voting power 3) Updated offer price (sometimes you even see LOWERED offer went through… will discuss later). Also, there are few deals announced over a year old but still didn’t reach definitive agreement, which I count them as failed. And also a few announced too recent, thus still in process which I didn’t count in (Successful column being “?”).

Some quick rundown: overall 27 of 37 (73%) went through; CEO/Chairman led – 22 of 31 (71%); Non-CEO/Chairman led – 5 of 6 (83%); Buyer over 50% voting power – 11 of 12(92%); Buyer below 50% voting power – 16/25 (64%).

At the first glance, the probability is not so appealing, except for the Buyer over 50% voting power group (92%). Also, it’s surprising that CEO/Chairman led buyer group had lower probability to get the deals done than non-CEO/Chairman led group (most of the time PE firms). I was expecting a higher number due to the connection CEO/Chairman has both with board and management team.

Failed Deals’ Characteristics

All happy families resemble one another, each unhappy family is unhappy in its own way.

– Leo Tolstoy

A slightly modified version of the Tolstoy’s quote would be: All successful deals resemble one another, each doomed deal failed in its own way. Now let’s dig into each failed case and see if we can find some patterns, just so we could avoid them.

China Cord Blood [CO]

- Withdrew on 4/13/2017

- Buyer is a small HK health PE, may have small bargain power potentially prolonging the process

- Offer price ($6.4) was lower than the previous day close ($7.22)

- Capital structure has complication, like convertible.

JA Solar [JASO]

- Still in limbo, no withdrawal announced yet after 2 years

- Chinese market crashed in second half of 2015, making this type of deals unattractive due to lower valuation in home market

- Buyer (the CEO/Chairman) owns only 15.6% the company, and has no PE backer.

- Sued by a supplier, Hemlock Semiconductor, on 1/2015

- Price kept sliding since announcement, Mr. Market seemed to know something more.

Renren [RENN]

- Still in limbo, no withdrawal announced yet after 2 years

- Chinese market crashed in second half of 2015, making this type of deals unattractive due to lower valuation in home market

- CFO resigned in 12/2014

- Had Dutch Auction Tender Offer in 4/2015

- New CFO also resigned 7/2015

- Price kept sliding since announcement, Mr. Market seemed to know something more.

- Formed special committee very late, in 12/2016 (1.5 years after receiving the offer…)

21Vianet [VNET]

- Withdrew on 6/30/2016

- CFO resigned 6/2015

- SEC fraud complaint by Street Watchdog (a short seller) in 12/2015

- Issued convertible in 4/2016

Airmedia [AMCN]

- Went into definitive agreement stage in 9/2015, however had no progress since.

- Targeted by short sellers over fraud in 4/2015, with class action suits raised by shareholders

- Complex restructuring in the deal (contingent on selling 75% of the advertising business first to one of the buyers)

China IT [CNIT]

- Withdraw on 10/11/2016

- Private placement and warrants issued in 5/2015, raised $13.54 million

- Price kept sliding since announcement, Mr. Market seemed to know something more.

Momo [MOMO]

- Planning to go private not too long after IPO (12/11/2015), price was higher than IPO though.

- Surprising failed deal as it’s backed by high profile PE shops (Sequoia & Alibaba)

- Chinese market crashed in second half of 2015, making this type of deals unattractive due to lower valuation in home market

- Not like all other withdrawals (which has no explanation), the CEO/Chairman offered a letter explaining why (citing strategic reasons). The stock price seems to confirm the potential of the company.

Jumei [JMEI]

- Planning to go private not too long after IPO (5/16/2014) with price significant lower than IPO price, simply irresponsible business practice (ripping early shareholders off).

- Minority shareholders got aggravated.

Auto Home [ATHM]

- Management had less than 5% ownership, and more than 50% was owned by a single owner Telstra, an Aussie telco. The deal basically fell through when Telstra decided to not play along, instead sold all its stake to Pin An, a Chinese leading insurer and financial service firm.

- Price kept sliding since announcement, Mr. Market seemed to know something more.

Overall, one should look out for and avoid these traits:

- These withdrawals are deals with buyers owns immaterial % (thus not disclosed), which I suspect lower than 5%. In these cases, the buyer will need to make sure big stakeholders are all on board with their buyout plan, which seems to increase the uncertainty of the deals;

- Beware of short sellers & litigation, which usually means the company may have adopted certain imprudent (even unethical) practices. You don’t want to touch them even in arbitrages.

- Beware of companies that had to access capital markets via preferred, convertible, private placements or warrants, etc. Usually a sign of exhausted traditional financing methods. And going private requires much further financing, you figure how they would secure them.

- Beware of go-private deals not too long after the IPO (and with price lower than IPO price). In these cases, either the management are great value destroyer, or great scalper (they basically short the company to IPO shareholders and cover them in buyout deal with much lower price). Either way, there is high risk dealing with this type of people.

- Beware of management team turnover around the announcement, usually not good sign.

- If the price drops after buyout deal announced, stay away. Mr. Market may know more than you.

Timeline

Timeline of the deal makes differences as that determines the IRR, as well as opportunity cost (tied up of your capital, causing missing other opportunities).

On average, 27 successful deals took about 178 calendar days (153 days median) to reach the definitive agreement stage; and 306 days (273 days median) to close the deal. Without any complication, I would expect a straightforward deal like Changyou should take about similar time to close.

In terms of spread narrowing, we see on average the spread closed to 4.82% (4.6% median) on definitive agreement day.

Additional Risk – Lowered Offer Prices

As mentioned before, there are a few cases (MR, JASO, KZ, DANG) where the acquirers lowered their offer prices and some still managed to get both board and shareholders’ approval. Because these deals all had current CEO/Chairman as the lead of the acquirer, who owns significant portion of the whole company, they could manipulate the deal to this unfavorable direction (to other shareholders). The reason, however, is time specific. As all these four deals are announced in June or July 2015, with the expectation to re-list themselves back to Chinese market, the following market crash significantly affected their deal’s feasibility, thus a lowered buyout offer is needed (warranted they still had premium over prices before announcement) to make the deal happen. This would be detrimental to risk arbitrageurs as their entry point is usually the elevated level right after the deal was announced. In Changyou’s case, I evaluate the possibility of lowering offer is very low. Additionally, the company drastically raise their 2017 guidance [Link here] on 6/5/2017 due to the very well received new release “Legacy TLBB” game. On the contrary, I actually would expect a sweetened offer, if there are some active shareholders pushing for it.

Conclusion on Changyou

Based on analysis above, I see Changyou buyout deal’s probability of being abandoned very low as it has no common traits with these failed deals. I also think this deal genuinely makes sense to Chairman Dr. Charles Zhang. The possible exit strategy could be either 1) relist Changyou in China; or 2) merge it back to Sohu so Sohu could be valued as a game developer and operator (similar to NetEase [NTES]). Bottom line, if the deal go through I make the 8% spread; or it doesn’t and I get back a business I had favorable view and believe its long-term potential. For now, it could be an additional cash parking position for me.

Disclosure: I long CYOU.

May I know what is your latest opinion now? With the special dividend of 9.40. Interestingly the price did not move much..

Hi Mike,

I’m already out CYOU, with heavy disappointment on Zhang’s series of decisions. In short, my latest view is that CYOU is a unloved middle child of Zhang, and its shareholders may be at risk of being thrown under the bus. It clear that all Zhang wants from CYOU is its cash, which he will be using for fund other cash-burning businesses under parent Sohu (mainly Video). It looks unwise to me to tap that cash using special div(at cost of taxes), since he is planning to buy out CYOU anyway (so he could’ve borrowed money, buy it out and get direct access to that cash, at cost of only interest)… maybe due to the repayment obligation of the CYOU-SOHU credit facility (otherwise, SOHU will have to surrender some class B shares to CYOU which were used as collateral). Now the cash is drawn from CYOU, Zhang’s incentive of buying out of CYOU may be largely decreased. Event it materializes, I think the new offer will be lower than the previous offer ($42.1) less special div ($9.4) = $32.7… Just my two cents.

Thoughts on SOHU/CYOU today? I wrote a piece on CYOU earlier on SeekingAlpha. CYOU seems ridiculously cheap for the cashflows it throws off with upside from games in pipeline. SOHU seems even cheaper with sum of the parts analysis (Sohu video set to break even by the end of the year too).

I agree SOHU/CYOU weren’t interesting after the buyout announcement/Dividend.I sold my positions after the announcements and bought in more recently. Overweight both positions as of today.

Here’s my quick analysis on SOHU today.

Sohu’s price March 21, 2019: $17.50

What’s SOHU Worth today? $32.70 – $43.76

Here’s a simple sum of the parts analysis:

Base Scenario:

Sohu SOTP ($681M MCAP @ $17.50/share):

Sogo stake (33%): $782M

CYOU stake (67%): $637M

-200M Holding co liabilities

NET Position $1.219B (Public securities)

(39m shares outstanding)

NAV (assigning $0 value for Sohu video/media business): $31.25 /per share @ market prices for equity.

Alternative Scenario

NAV if CYOU bought out at @ $32.70 (Proposed buyout – dividends)

Sogo stake (33%): $782M

CYOU stake (67%) @ $32.70/share: $1,124M

-200M Holding co liabilities

net position $1.706B

NAV (assigning $0 Sohu video/media business): $43.74

$32.70 – $43.76 Value range.

Even the ‘base’ scenario is is extremely conservative. I’m assigning ZERO value to Sohu’s main business (video/portal) which is the 12th most visited website in the world and the 5th most visited in China. It generated $232M in revenues in 2018. Sohu also invested a lot into original content (which I consider a waste of shareholder money, but it still has some value. Maybe half of what they put in. SOHU video should breakeven by the end of the year). At the bare minimum Sohu’s video/media business is worth $250M+, but lets just discount it entirely.

$32.70 – $43.76 assuming zero upside in SOGO, which is an interesting play on AI and backed by Tencent. Safe play too. Profitable and has $1b in net cash, so it’s pretty cheap.

CYOU is trading at ~4x EV. The CYOU/SOHU complex just seems too cheap to ignore.

Hey Omer. I’ve checked your works and think they are good quality reads.

First on CYOU buyout, I think Zhang wanted its cash (for SOHU), which he already got via the special dividends. I don’t see why he would want to honor it after all.

I don’t disagree with your valuation, which is why it attracts me at the first place. For value gap to close, there has to be some manifestation (no one knows when though). Given what I understand of Charles Zhang, I’m doubtful on his drive to 1) close the value gap & 2) continue creating value for Sohu’s users. Zhang had gone through a mid career crisis and suffered severe depression circa 2011 (he had trouble accepting Sohu became obsolete and himself as the 1st generation of Chinese internet entrepreneur under-achieving his peers by large margin). He had to retreat to Buddhism for 2 years to rebuild his mental health. After this retreat, he seems to be mentally stable, however appears to lose the drive and competitiveness as an entrepreneur. He hasn’t laid out convincing vision to make Sohu relevant again. He might be fine just let them to roll down the hill as is…

So SOHU/CYOU certainly can be plays going from “very cheap” to “less cheap”, but my faith in them to go to “fairly valued” is largely dimmed. Without the vision to turnaround, in long term, it might be the value gradually converge its lower price…

SOGO is different, CEO Xiaochuang Wang seems still quite driven and they have Tencent as another large shareholder. They also have some good progress on AI front, albeit with less clear path of pivoting business model though.

Hope it’s of help.