As an old saying says, “you best teacher is your last mistake.” However what’s challenging for value investors is that it’s very difficult to realize you’ve made a mistake to start with. As you are always going against herds, you’ve already made “mistakes” in others’ eyes, meaning you are left alone to make the judgement. Plus, you have to re-convince yourself about your verdicts when the name keeps going down after your purchases, or if the names move higher you just cannot stop feeling good about yourself, either way it’s really hard to maintain an objective view on your own past decisions.

Market recently has seen some big failures on names backed by some legendary value investors. Although may not be able to learn the lesson as deeply as the investor themselves do, I found these are great case studies nonetheless.

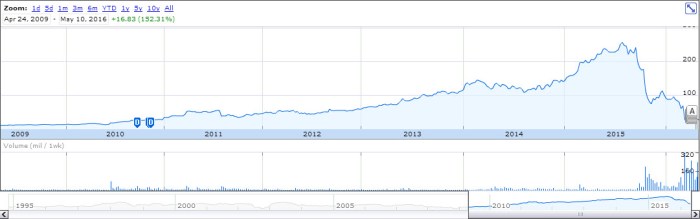

Bill Ackman – Valeant

The Canadian drug maker has seen it’s price on a rocket since Ackman teamed up with former McKinsey consultant J. Michael Pearson to reign the firm. The name got so heated in the hedge fund society that it even got buy-in from one of the the most well regarded value investor Sequoia Fund (where Warren Buffet directed his investors to, after he closed his partnerships back in 1969).

The rises and falls of Valeant is a fascinating story, which on hindsight you would find many “signs”. I cannot tell the story better than AZ Value, who published some great summary and analysis on VRX at his blog here. I highly recommend reading them thoroughly.

Some of the lessons I learned from this piece of history:

- Be very careful about acquisition fueled growth company with low R&D expenditure/CAPEX, as that tells you one thing: the company is trying to commoditizing everything they could find. That is not a sustainable strategy. Things are even worse if these acquisitions are funded mostly by debt.

- Complexity may be a good thing in creating market inefficiency. However, as an investor, you should avoid to feel overconfident that you are the only one who can understand the complexity. Preferably, a good business with complex models should have better than average investor relation communications (to make things less complex to understand). If you find the company’s disclosure/communication confuses you more, that’s possibly the management is trying to mislead the market.

- Integrity and morality of the executives matters. With the power at hand, executives really have countless ways to act in self interest even with the corporate governance structure we have today. Many of these practices are not illegal, take Valeant’s example, CEO J. Michael Pearson decided to raise drugs prices aggressively soon after acquiring small drug makers. According to Pearson, it is to ultimately benefit shareholders, however you can say in some way it’s benefiting his stock options package. This aligned interests seem to be working fine, except it will leave the patients disadvantaged, which is really a immoral practice against drug makers’ mission to use innovation to cure diseases and to improve general public’s living quality. On individual basis, these decisions may not seem to be big deals, but many of these unethical practices accumulated together may lead to an avalanche.

David Einhorn – SunEdison

SunEdison, another hedge fund darling, has seen a stellar performance on it stock, only in a even faster pace than Valeant. Its stock more than tripled in less than two years from mid 2013, reaching high of $30, however dropped like a rock triggered by a liquidity crisis from mid 2015 to worth almost nothing now.

This WSJ piece and this John Huber’s piece did great jobs summarized the rises and falls of SunEdison. Interestingly, there are many similarity in these two companies’ falling.

- Debt fueled aggressive expansion & acquisition is a double edged sword, like seen in Valeant case. SunEdison adopted a very controversial financial engineering practice called “yieldco”, which basically is using spun off entities (who will buy whatever products the parent company sells to them) as revolving facilities. Be careful what a firm is buying and how much it pays for assets when they have “easy” money, a key factor leading to SunEdison’s burst is that they bought many bad assets or overpaid many OK assets, simply because they probably felt they had to get some deals done with the abundant funding. Also be careful about the liquidity when companies use excessive debt (including these financially engineered debt) to support growth, a small headwind will blow the whole thing up just as using leverage to investing.

- Integrity and morality of the executives matters [again]. To start with, Chatila’s decision to push many these bad deals through is not a responsible practice as CEO, and you can easily link the rationale behind it is to maximization his own short term paycheck. Without a better incentive mechanism, it is really only the executive’s integrity which can direct him/herself to make responsible and long-term focused decision. Additionally, the liquidity problem for SunEdison probably was known internally for long since we’ve seen many executives resigned or got let go before it finally exploded. Screwing up the business is one thing, but trying to deceiving investors really brought it to a new low from moral standard perspective. Executives stated on Nov. 11 conference call that they had “sufficient liquidity” with $1.4 billion cash handy, however later investigation found out that there was only $90 million cash and all the rest are restricted loans that can only be tapped with some high quality projects as collateral (which they don’t really have).

Mohnish Pabrai – Horsehead

There is much less coverage on Pabrai and his position in Horsehead Holding, a recycling zinc & nickle-based product maker. Since I am reading his book these days, I read the other day that he recently sold out all his holdings in this doomed company. Here I endeavored to explore why Pabrai initially entered this position and why it didn’t work out.

Horsehead recently filed chapter 11 bankruptcy, under a liquidity crisis. Based on Pabrai’s 13F filings, he had Horsehead as holding as back as May 2012. By going through the company’s old filings, this Barron’s article and this VIC post, I think there are following attractive traits of this firm:

- Considerable moat in terms of barrier of entry for competitors (capital intensive to set up similar recycling facilities), and its dominating position in processing electric arc furnace (EAF) dust, a toxic by-product of the steal industry.

- New state of art recycling facility upcoming: in 2009, Horsehead started to build a new recycling facility in Mooresboro, N.C. using state of the art process and technology. It will not only increase the capacity, but also decrease the producing cost substantially. And seems the upside of the new facility was not priced in fully, as pure financial numbers showed a negative picture of the company.

So how it went wrong? In short, couple of adversity coming together. One hand, global commodity industry started a seemingly abysmal downturn from mid 2014, causing zinc price to drop, hitting through Horsehead’s break even point. On the other hand, the new facility was plagued by some “design and engineering problems”, causing it could never ramp up to full capacity until a further $82 million investment to get it fixed. All in all, it seems like a good investing opportunity standing in the point of time, but it just got hit by a perfect storm. Interesting readers can read further on this good piece from Pittsburgh Business Times for more history of the rises and falls.

Some of the lessons I learned from this piece of history:

- Be careful about leverage [again]. Liquidity should be estimated more conservatively.

- For firm that had profitability heavily relying on very few factors (either commodity price, or concentrated client base, etc.), make more conservative assumptions and try to size the position more conservatively as well.

Among these three failed investments of three great investors, there are some common takeaway useful for part time investors like me.

- Beware of overly aggressive acquisition/expansion, especially when they are done with debt as primary funding.

- Beware of the leverage and liquidity situation, and try to make conservative assumption.

- Don’t buy in too much of companies’s slides and corporate communication. Try judge executives integrity by doing more background research. If not possible, try to find data back favorable corporate communication before buying in.

- For investors ourselves, keep modest, do your best to distinguish between persistence (where you think the loss is temporary and the name will come back up) and hubris (where you are not sure if the loos is temporary but don’t want to admit you were wrong).

- Lastly, we all make mistakes and we will all move on. The important thing is we learn from our mistakes, don’t need to be too obsessed with the loss. Investing is an odd game after all, you will do fine as long as you make more wins than losses.