Disclosure: I established a long position in NXRT on 4/4/2016.

First of all, I want to thank following posts drew my attention to this name. It caught my eye first that Michael Burry held it as his biggest position.

Michael Burry’s SEC 13F filing

Clark Street Value post about NXRT

Value Investors Club post about NXRT

After I made my trade, I wanted to write something about it, however I noticed there are this Gurufocus article on 4/4/2016 and this Seeking Alpha article published on 4/5/2016 already did most of the job and shared some of my views. Thus, I will be brief on the upside as you will be able to get them from articles listed above, and will try to dig more into the downside.

Short pitch: NXRT is one of the few REITs using “value add” strategy on class B properties. The management is very determined to execute on this strategy and thinks the market didn’t get them (small cap, spun off a year ago, only 2 analysts from some boutique sell sides covering them). In my view, this firm is actually a flipper partnership under a REITs cover (to avoid corporate level tax), and their flipping strategy seems to be very lucrative (if it works out).

Following I will touch some of the red flags that people dislike the most (and I disliked initially):

-Leverage: Over 70+% debt/EV. Total debt amounts $711 million, part of that a $29m bridge loan from KeyBank to facilitate the down payment for two properties in mid-2015 and will be due in full mid 2016, and the rest are all mortgage. This tells me two things: 1) they are out of capacity to do more acquisitions 2) majority of the debt are mortgage.

The key question I ask to assess the risk is: will it and how will it explode? Look at their obligations and commitments section from 2015 10-K, you will see from 2018 on they will need to pay a lot more principal. Combining with interest payment & dividend payment (to maintain REITs status, just use this year’s 13 million assuming no change), it already exceed the Net Operating Income (even after adjustment using the rent growth rate after rehab). Additionally, I found the average mortgage terms are 7.6 years. So there is NO way the firm can pay down these debts with their operation.

However it still doesn’t mean that the firm is going to burst, as they can simply sell some properties (and that’s when I started to wonder maybe the whole intention is to sell them in short term). Then the question becomes: will they have to sell them at discount? Very possibly not, because 1) the US housing market condition is generally going upward and 2) I think the firm’s untold real intention is to “flip” so the properties they picked should be the ones are easy to sell. (you will find below more evidences for efforts the management made to make it “easy to sell”).

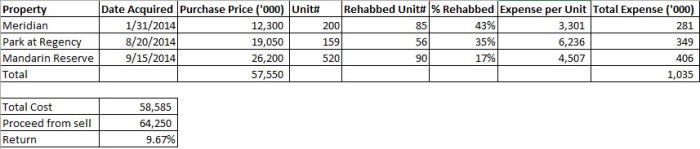

One would argue the reason 2 is my pure speculation, yes that’s right, and that’s why I waited until now to make the investment because I have found some evidence about the effectiveness of the management’s ability to dispose property. Disclosed on the most recent conference call, the firm already sealed deals to sell 3 properties (@ 6% cap rate, and 10% higher than purchase price + rehab cost, see calculation below) to pay back the 29 m bridge facility matures mid 2016. With some down payment % assumption and interest rate assumption (they said avg. around 2.67%), you can get a rough idea of what’s the return on equity (should be north of 20%). I think this is a good example demonstrating the firm’s ability to executing dispositions even under debt payment pressure and it might be a catalyst for the market to realize the value of the firm.

-Floating rates debt: Almost all the mortgage of NXRT is floating rates and many people (from the comment section of these articles) questioned the sustainability of the firm. If you listen to the conference call for Q4 and FY 2015, you will pick up this hint: the firm doesn’t expect to hold the assets too long, because floating rates mortgage are more flexible in prepayment and makes the assets more appealing for potential buyers. Evidence # 2 here for “making it easy to sell”.

Let’s suppose there will be a near turn rate hike, and the interest payment for the firm increases to a level that cannot sustain. Still, the firm can deleverage by selling some more properties, and the implication for equity holders is that you are not able to make that much money (compared to the low rate environment). The difference (than principal payments) is that rate hike are harder to predict, so the reaction time for the firm will be much shorter. The worst scenario is that the firm may need to sell at distress and incur some loss, but there can be other ways to handle it (e.g. get another bridge loan, or use more cash from operation however that would impact the REITs status), anyway the point is that it highly possible won’t burst.

-External management: I also see people questioning this and said it creates conflict of interest between principal and agent. I partially agree with it. However, you have to note that both the property manager (BH Equity) and the advisor (NexPoint Advisors) are affiliate, especially the advisor who is ran by the same group of officers of the REITs. So it’s really left and right pockets of a same person.

This is a very unique (and strange) setup, and does introduce conflict of interest. The officers can basically use the REITs as an ATM by charging the advisory fee (albeit capped @ 1.5% of the asset value) regardless how well or bad the REITs business operates. So it makes sense now why they decided to acquire assets even using bridge facility (because that increases the asset value under management).

However, I think the REIT should be the favorite kid given the possible payoff and management’s ownership. Management holds big position in the REIT (10K didn’t disclose this time but from previous filing I found the president James Dondero held 11.4% and the parent company Highland Capital held another 11.4%) and they are still buying more (check Form 4). The potential equity return should dwarf the potential growth in advisory fee, so I think it’s safe to assume that the management will take care of the REITs and its shareholders (i.e. themselves).

The firm’s desire to refrain from internalizing any property management and operation is also evidence #3 that their intention is “make it easy to sell”, just so the potential buyer don’t need to worry about organization integration and can simply include the properties into their portfolio and realize synergy.

-“Emerging growth company” exemption under JOBS Act: No one mentioned this as far as I saw. But I’m particularly interested in learning how transparent and open the firm is about its strategy and performance. When I first saw this from their 10K I gave a frown because it would mean the firm doesn’t need to disclose information timely, if not at all (that’s why they can file 10K with the compensation and ownership section blank and can file them later). However, I later came across their investor relationship website (which is quite investor friendly) and also listened a few conference calls. I think I will give it a pass and can take it as a genuine reaction because of lack of resources.

So after looking at all points above, it’s obvious to me that the whole business plan is to buy, rehab and sell. All of the red flags don’t appear as bad as they look initially (some are even positive for setting things up for sell) after I changed my view of the business plan. The key assumption I made is the effectiveness of the firm’s ability to disposition and it’s yet to be confirmed by numbers from the filings. Once the firm starts more disposition activity and the numbers make to the filings, more investors will get it. I see that as a short term catalyst.

Depending on how the firm is going to sell (either sell by properties or sell the whole firm), I will determine when to exit. Either way, I would hope the value can be reflected in 1-2 years, as the management mentioned that they will start more dispositions in 2016.